Harnessing Asia’s dividends: Investing in income and growth opportunities

The case for Asia dividend investing

As interest rates have shown volatility over the past year with a slower pace of decline, investors are increasingly turning their focus towards reliable sources of income. At the same time, a weakening US dollar and geopolitical challenges—including persistent tariff disputes—are adding layers of uncertainty to global markets.

Amid these dynamics, Asia’s dividend landscape has emerged as an appealing option for those seeking income and diversification. With US AI stocks reaching stretched valuations, investors are seeking to rebalance their portfolios by exploring Asia's compelling growth opportunities and favorable valuations, increasingly robust shareholder-focused reforms, and strong corporate fundamentals. In this environment of uncertainty, Asia offers the combination of income prospects and long-term growth opportunities.

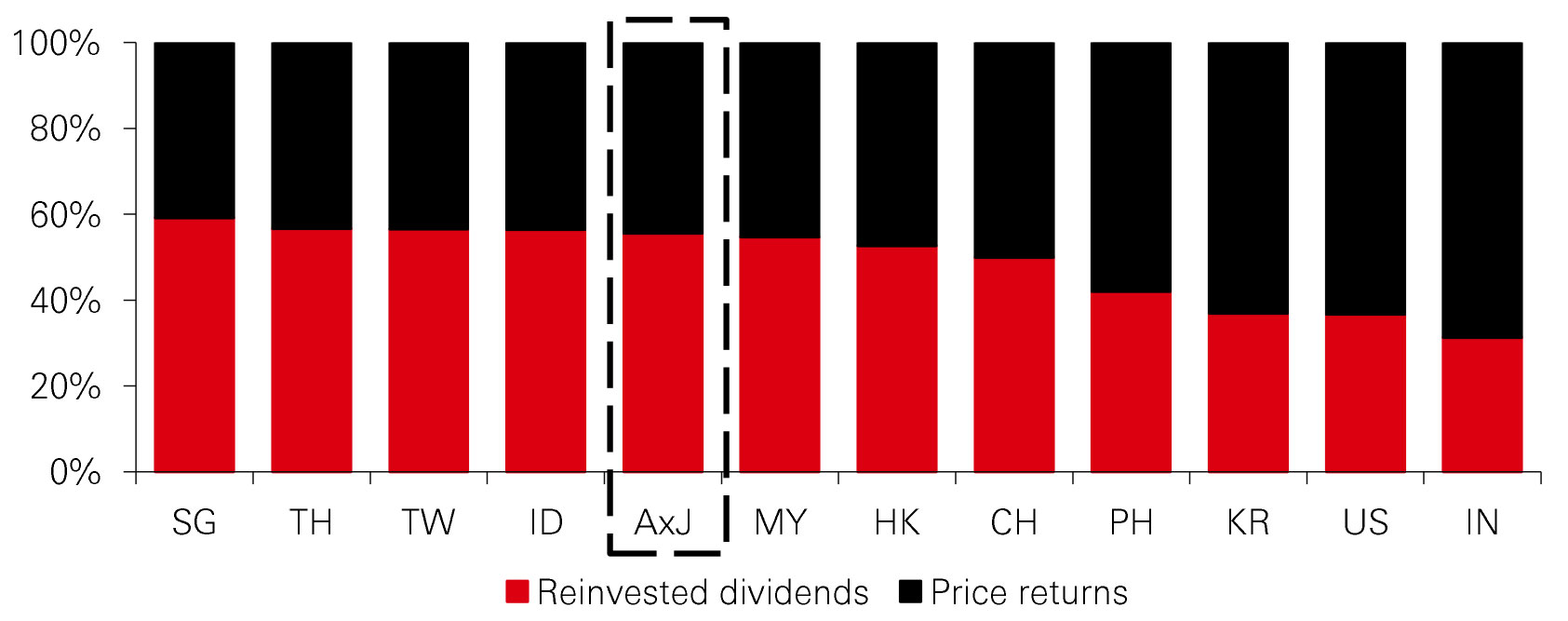

Over the past 25 years, dividends have been a central pillar of Asia’s investment appeal, accounting for more than half of the region’s total returns—a clear testament to its income-generating strength. For perspective, dividends from Asia ex-Japan have contributed 56 per cent of total returns, significantly outpacing the 37 per cent contribution observed in the US (Fig 1). Recent government policy initiatives, such as those in Korea and China, mean that using dividends as a way to enhance shareholder returns in Asia has grown increasingly compelling.

Fig 1: Dividends contribute a substantial share of Asia’s total returns

Contribution to total return between 2000 and 2025

Using FTSE indices. Source: FTSE, as of December 2025.

Note: IN – FTSE India, KR – FTSE Korea, TW – FTSE Taiwan, TH – FTSE Thailand, ID – FTSE Indonesia, SG – FTSE Singapore, HK – FTSE Hong Kong, CH – FTSE China, MY – FTSE Malaysia, PH – FTSE Philippines, US – FTSE US, AxJ ‒ FTSE All-World Asia Pacific ex JP, AU and NZ.

A clear path to boost shareholder returns

Korea

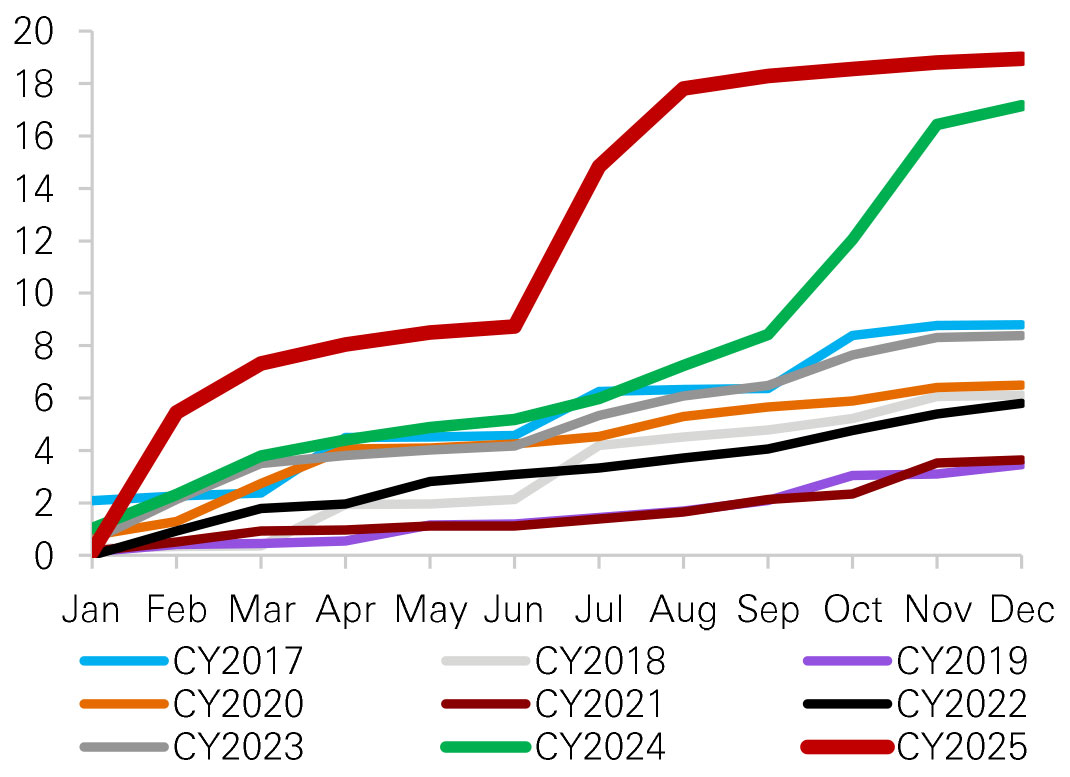

Korea’s commitment to corporate governance reform is paving the way for enhanced shareholder returns. Companies are responding to policy shifts by deploying capital more efficiently, increasing dividends, and initiating stock buybacks. Noteworthy among these reforms is the “Value-Up” programme, launched in 2024, which aims to address the undervaluation of Korean equities by encouraging corporates to adopt stronger shareholder return policies.

Korean companies spent KRW 18.94 trillion (USD 13.2 billion) on share buybacks in 2025, an increase from KRW 17.15 trillion (USD 12.0 billion) in the previous year (Fig 2).

In December 2025, Korea’s National Assembly passed a bill introducing separate taxation for dividends, designed to incentivise higher corporate payouts. Companies that either exceed a 40 per cent cash pay-out threshold or maintain cash pay-out ratios above 25 per cent while increasing dividends by more than 10 per cent year-on-year will qualify for favourable tax treatment. This reform is expected to serve as a catalyst for dividend increases, as firms seek to benefit from the newly applied tax regime beginning in 2026. With such targeted initiatives, Korea offers a fertile landscape for income-focused investors.

Fig. 2: A significant increase in share buyback activities in South Korea since 2024

YTD cumulative buyback announcement (KRW trillion)

Source: FactSet, Goldman Sachs Global Investment Research, December 2025.

China

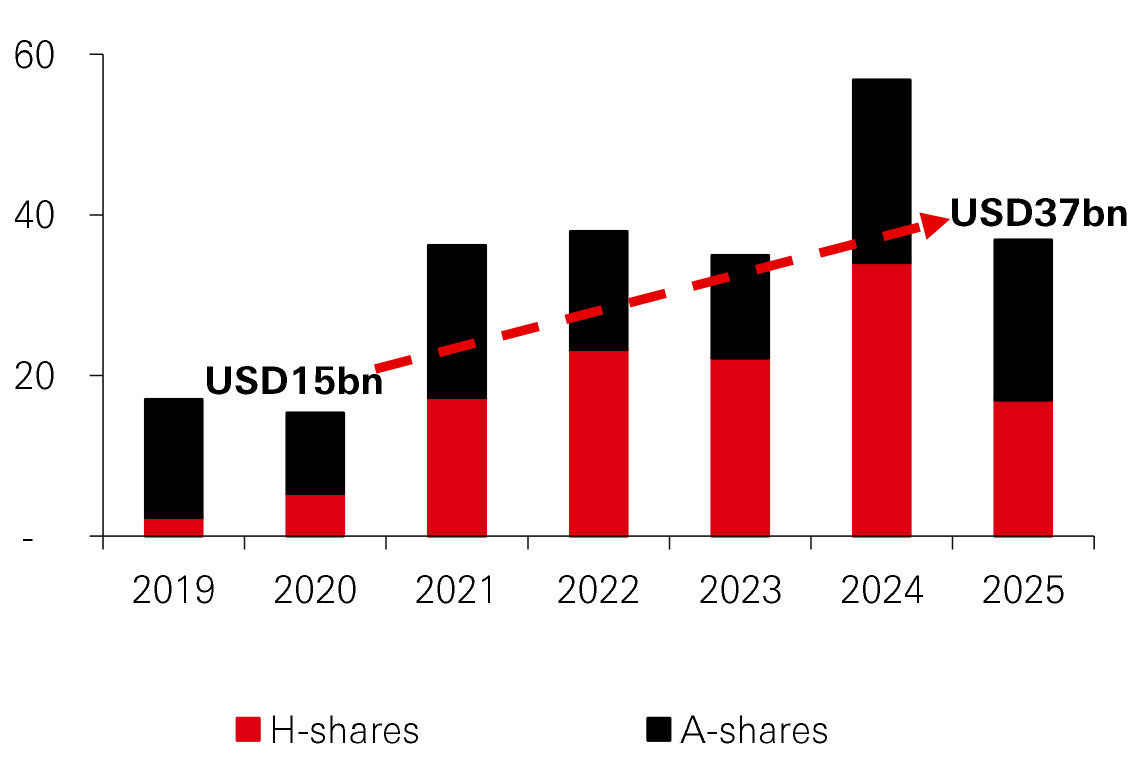

Since early 2024, Chinese authorities have implemented polices to encourage listed companies to prioritize shareholder returns. The China Securities Regulatory Commission (CSRC), for instance, encourages companies to pay dividends multiple times per year, rather than just at year-end.

Additionally, profitable A-share companies with low payout ratios face regulatory scrutiny, with major shareholders prohibited from selling shares unless dividend policies are improved. Driven by the policy initiatives, share buybacks soared to USD 57 billion in 2024 from USD 15 billion in 2020 (Fig 3.) These measures have made a clear impact.

On the other hand, in 2024, the dividend payout ratio in China’s market reached 39 per cent, up from 37 per cent the year prior and far above the 10-year average of 31 per cent1. Nearly 900 companies-initiated share buyback programs for the first time in the last five years. These developments highlight China’s increasing commitment to fostering an income-friendly investment environment, making it a compelling market for dividend seekers.

Fig. 3: Share buyback activities of Chinese equities

USD bn

Source: Wind, Bloomberg, HSBC Global Research, December 2025. H-shares refer to Chinese companies listed on the Hong Kong Stock Exchange, while A-shares represent Chinese companies listed on stock exchanges in Mainland China.

Solid fundamentals in Asia

Solid fundamentals

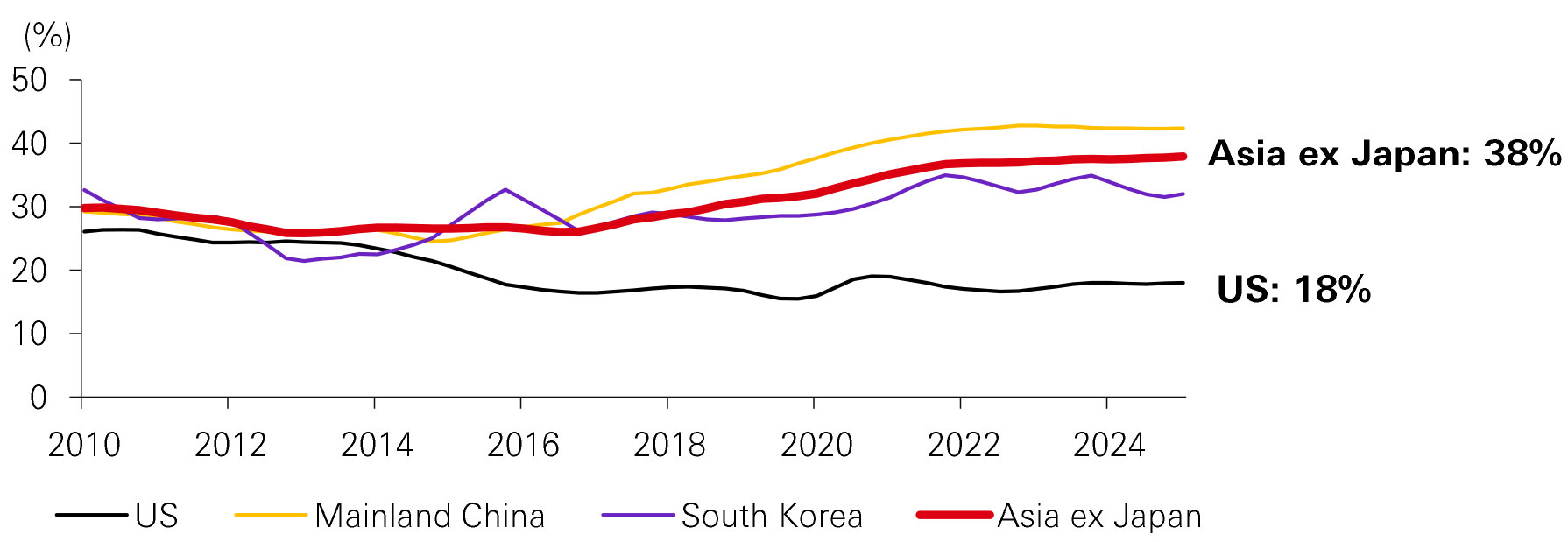

Beyond targeted policy reforms, the broader financial health of Asia’s companies is also improving. As of 2025, nearly 40 per cent of Asia ex-Japan companies are net cash positive, compared to just 30 per cent in 2010 (Fig 4). This enhanced cash position provides firms with greater flexibility to optimize their balance sheets and reward shareholders. Additionally, the region’s earnings growth is projected to accelerate from 11 per cent in 2025 to 30 per cent in 2026, according to data complied by Goldman Sachs Research in February, further boosting the potential for higher dividend payouts.

Navigating market volatility with bottom-up stock picking

While geopolitical tensions and policy uncertainty continue to drive market volatility, Asia’s increasing emphasis on shareholder returns offers investors a powerful counterbalance. In this environment, bottom-up stock picking becomes critical to identifying companies with the potential to deliver both income and consistent alpha.

Asia’s dividend story is well underway, strengthening the case for income-focused investing. For income-focused investors, the region offers not just a stream of dividends, but also the opportunities for long-term value creation.

Our Asia High Dividend strategy is centered on identifying high-quality companies with strong balance sheets and sustainable growth potential, offering investors income and long-term opportunities in one of the world’s most dynamic regions.

Fig 4: Percentage of companies which are net cash positive

Source: FTSE Russell, Factset, HSBC Global Research, data as of December 2025

Note: US – FTSE US, Mainland China – FTSE China, South Korea – FTSE Korea, AxJ ‒ FTSE All-World Asia Pacific ex JP, AU and NZ.

This commentary has been produced by HSBC Asset Management to provide a high level overview of the recent economic and financial market environment, and is for information purposes only. The views expressed were held at the time of preparation; are subject to change without notice and may not reflect the views expressed in other HSBC Group communications or strategies. This marketing communication does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. The content has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. You should be aware that the value of any investment can go down as well as up and investors may not get back the amount originally invested. Furthermore, any investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in established markets. Any performance information shown refers to the past and should not be seen as an indication of future returns. You should always consider seeking professional advice when thinking about undertaking any form of investment.

Source: HSBC Asset Management, as of February 2026.

Note: 1: Goldman Sachs Research, data as of 7 January 2026

Past performance does not predict future returns. Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecasts, projections or targets. The views expressed above were held at the time of preparation and are subject to change without notice. The information provided does not constitute any investment recommendation or advice. Diversification does not ensure a profit or protect against loss. For illustrative purposes only.

Important information

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. Past performance contained in this document is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in Emerging Markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Mutual fund investments are subject to market risks, read all scheme related documents carefully.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Global Asset Management Global Investment Strategy Unit at the time of preparation, and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Global Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity.

We accept no responsibility for the accuracy and/or completeness of any third party information obtained from sources we believe to be reliable but which have not been independently verified.

Investment involves risk. Past performance is not indicative of future performance. Please refer to the offering document for further details including the risk factors. This document has not been reviewed by the Securities and Futures Commission.

HSBC Global Asset Management is the brand name for the asset management business of HSBC Group. The above communication is distributed in Hong Kong by HSBC Global Asset Management (Hong Kong) Limited.

Copyright © HSBC Global Asset Management (Hong Kong) Limited 2026. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Global Asset Management (Hong Kong) Limited.