Asia multi-asset capabilities

Resilience and innovation amid global volatility

Read this article for insights into investment views across key Asian asset classes, along with Asia multi-asset allocation perspectives, amid a global environment of heightened uncertainty.Asia multi-asset perspective

Asia’s resilience with policy support and tech drivers

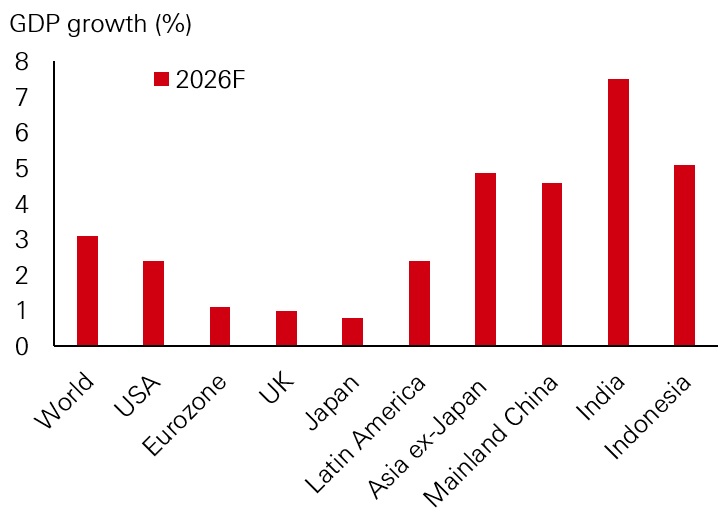

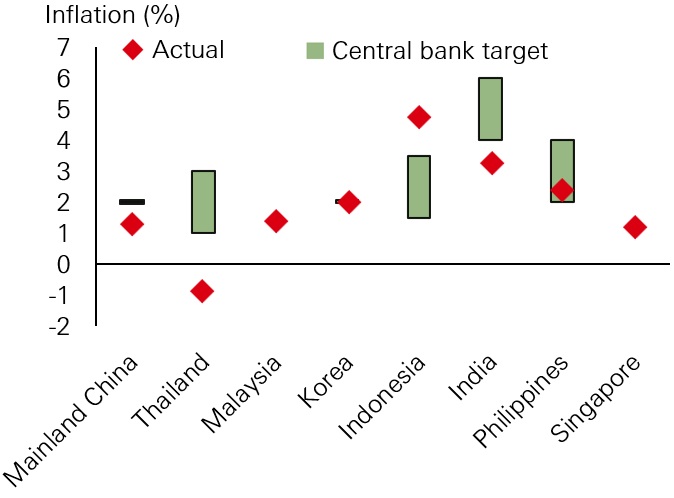

With 2026 now in full swing, Asian economies are showcasing resilience in the face of ongoing market uncertainties and geopolitical developments (Fig. 1 and 2). Tech tailwinds and domestic policy support should help provide a buffer against energy headwinds and global volatility.

Fig 1: Asia GDP growth relatively strong vs rest of the world

Source: Source: Bloomberg forecasts, HSBC Asset Management, as of 26 March 2026.

Fig 2: Inflation in Asia generally at central bank target/comfort zones in most

Source: Source: Bloomberg, HSBC Asset Management, as of 26 March 2026.

Policymakers in Asia are expected to remain vigilant against inflation and macro-financial stability risks. While most Asian central banks are likely to take a wait-and-see approach in their monetary policy, fiscal policy in the region should address the energy shock and potential spillovers to the economy – including through subsidies, tax cuts, import tariffs, and support for households and businesses. Policy measures are also expected to continue supporting the domestic economy and capital markets. Divergence across Asian economies in their growth and policy paths is likely amid local idiosyncrasies.

Despite this, the region remains well-positioned to reap productivity gains from AI investment and adoption. Asia continues to be a critical player in the global AI ecosystem, underpinned by its dominance in cutting-edge semiconductor manufacturing (such as in Korea and Taiwan) and innovative software development.

Overall, Asia assets continue to look relatively compelling: Asia bonds are supported by solid fundamentals and comparatively attractive all-in yields while Asian equities are backed by strong earnings growth and distinct domestic growth drivers. Nevertheless, we remain mindful of risks arising from geopolitical tensions, oil price shock, the US Fed’s rate cut path, concerns over the global growth outlook, and global trade policies.

Capturing Asia’s investment opportunities with multi-asset strategies

Asia continues to be a hotbed of investment opportunities while the region has also become heterogenous, where each market has its own distinct economic and policy structures. Given these varied drivers, our multi-asset strategies at HSBC Asset Management aim to ensure diversification and capture opportunities across asset classes, markets, and sectors. We manage various Asia multi-asset solutions with varying risk profiles and objectives, including conservative, income-focused, and growth-oriented strategies, which aim to be suitable for a broad array of client risk and return objectives.

Income focused strategies

In our Asia multi-asset income focused strategies, we aim to capture upside potential from equity, income from dividend stocks and attractive yields from bonds. The case for a multi-asset income strategy is well supported by comparatively high yields in Asian fixed income and the substantial contribution of dividends as a proportion of total returns in Asian equities.1 Recent government policies, such as those in Korea and China, also indicate that using dividends as a way to enhance shareholder returns in Asia has grown increasingly compelling.

From an asset allocation viewpoint, we maintain a preference for equities over fixed income amid robust corporate profits in the region. Meanwhile, in fixed income, we expect Asia investment grade credit to remain resilient given the solid corporate fundamentals, and Asia domestic bonds to be backed by a favourable macro backdrop and relatively high yields.

Dynamic and diversified

Building resilient and truly diversified multi-asset portfolios depend largely on effective asset allocation. Our dynamic asset allocation and disciplined portfolio construction based on proprietary portfolio optimisation and risk budgeting helps our strategies aim for optimal risk-adjusted returns and is designed to capture various dimensions of diversification. Beta diversification is managed and spread across asset classes and investment styles, while our granular approach to asset allocation helps unlock alpha in specific market segments.

We have a proven and established investment process that relies on extensive research resources, combining quantitative and qualitative inputs to ensure a disciplined and repeatable approach to multi-asset investing.

Key equity asset class views

Asia Pacific ex Japan equities

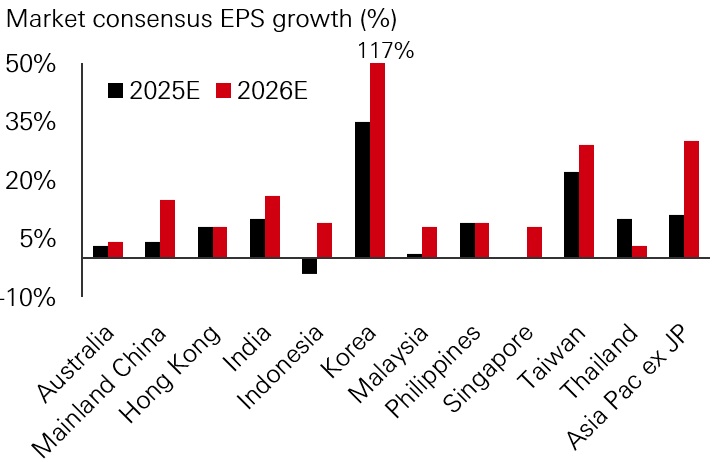

Asia’s overall economic outlook remains favourable for equity markets, owing to regional trade integration, technological advancement, resilient domestic demand, and supportive policies. The earnings outlook for the asset class remains solid, with growth forecasted to accelerate from 11 per cent in 2025 to 30 per cent for Asia Pacific ex Japan equities in 2026, led by strength in Korea and Taiwan (Fig. 3).

Fig. 3: Earnings growth remains solid

Source: IBES, Goldman Sachs Research, 21 February 2026; Asia Pac ex JP refers to the MSCI Asia Pacific excluding Japan index.

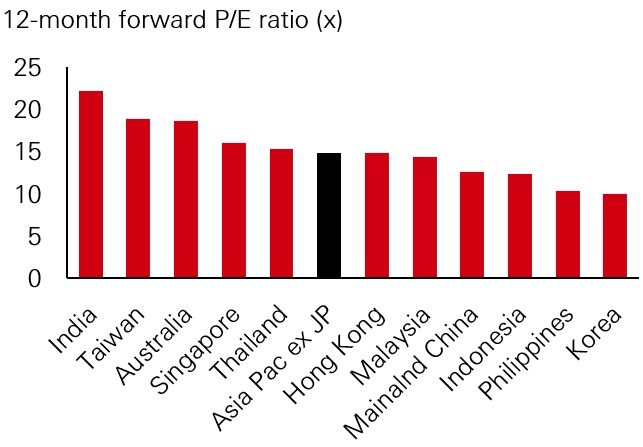

In terms of valuations, 12-month forward P/E continues to stay reasonable overall, trading at 14.8x (Fig. 4). The overall outlook for Asia Pacific ex Japan equities remains constructive, with markets offering broad sector diversification and high-quality growth opportunities. However, potential risks which we closely monitor, could stem from geopolitical events, US-China relations, AI super cycle marked by elevated valuations, and trajectory of the monetary cycle.

Fig. 4: Asian markets’ valuation underpinned by strong earnings growth and solid fundamentals

Source: MSCI, Bloomberg, Goldman Sachs Research, 21 February 2026; Asia Pac ex JP refers to the MSCI Asia Pacific excluding Japan index.

Korea and Taiwan equities

Korea and Taiwan are markets with high contribution to AI innovation and may be poised to benefit further following a strong year. Any acceleration in global AI capex is positive for these markets, with both having high exposure to key semiconductor and IT hardware segments that benefit from increased spending on AI servers and data centers. This includes Korea’s strength in memory and high bandwidth memory (HBM) and Taiwan’s concentration in advance chip manufacturing. Additionally, further progress on corporate governance reforms in Korea would be well received by investors and could potentially boost market sentiment. Both Korea and Taiwan equities have also been able to maintain strong momentum in earnings upgrades.

Indian equities

Indian equities are expected to benefit from the domestic economy’s strong structural growth drivers, the government’s ongoing reform initiatives – including last year’s overhaul to the Goods & Services Tax (GST) regime, and a continued structural shift in household savings. India has also successfully reached trade agreements with the United States – in addition to the recent trade deals with the European Union, addressing long-standing uncertainties and strengthening its position to navigate geopolitical headwinds effectively. Indian equities’ earnings outlook is improving, despite clear sectoral divergence. While valuations are relatively rich, the premium over emerging markets has fallen to 65 per cent, closer to its long-term average of 51 per cent.2

Chinese equities

China’s supportive macro policies combined with its export and manufacturing competitiveness should help provide a cushion against potential headwinds. Innovation should remain a key driver of Chinese equities, with growing AI adoption and tech breakthroughs expected to enhance productivity and benefit AI-related names. Capital flows from domestic investors should also continue to drive the market. Valuations continue to look relatively attractive. Forward P/E for the MSCI China Index (12.6x) trades at a significant discount versus the S&P 500 (22.2x) and other major markets.3 Fundamentally, corporate earnings are seeing signs of stabilisation, with a structural improvement in return on equity (ROE), which has been underpinned by corporate driven actions, shareholder return initiatives, government support for the private sector, and new tech leaders.

Japan equities

Japan equities’ valuations are compelling versus other developed markets, bolstered by continuing corporate governance reforms. Domestically-oriented sectors look favourable on increasing fiscal support, but the earnings outlook for exporters/cyclicals remains highly sensitive to global macro and trade conditions, with additional downside risks from higher Japan government bond yields and a stronger yen.

Key fixed income asset class views

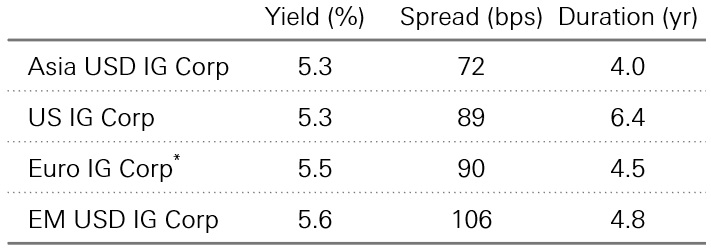

Asia investment grade credit

Returns for the Asia investment grade credit market in 2026 may moderate, reflecting the US interest rate outlook and more limited scope for spread tightening in the market. However, solid credit fundamentals continue as a key driver of performance, thanks to the region’s robust macro environment. Fallen angel risk has continued to subside, with only about 0.2 per cent of the Asia investment grade market downgraded to high yield in 2025.4 Strong credit profiles of investment grade issuers should help support resilience through periods of market volatility. At the same time, credit spreads are at historically tight levels, though duration remains shorter than peers (Fig. 5).

Fig. 5: Investment grade bonds valuations

Note*: Euro IG Corp yields listed are USD hedged.

Source: JPMorgan, BofA, 26 March 2026.

We are seeing investment opportunities in select regional bank and insurance subordinated debt, mainland China TMT, Indonesia commodities and utilities. We remain mindful of risks arising from uncertainties around the US Fed’s rate cut path, lingering concerns over the global growth outlook, and global policies.

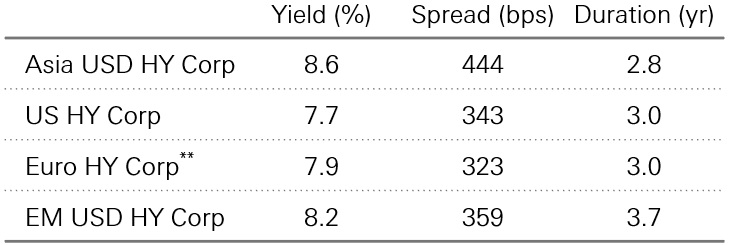

Asia high yield credit

Asia high yield default rates have fallen back to the low levels seen prior to 2020 while idiosyncratic risks over the past year have not meaningfully spilled over into the broader market.5 However, we continue to pay attention to issuer-specific issues, which may cause short-term market fluctuations.

While credit spreads are tight compared to history, Asia high yield bonds offer carry and spread compression potential compared to global peers (Fig. 6). We continue to prefer investment opportunities in mainland China industrials, India commodities and cyclicals, select India renewables, India financials, regional high yield commodities, frontier sovereigns and select banks.

Fig. 6: High yield bonds valuations

Note**: Euro HY Corp yields listed are USD hedged.

Source: JPMorgan, BofA, 26 March 2026.

Asia local currency bonds

Asia local currency bonds are backed by sound fundamentals in Asian economies and relatively high real yields. The local inflation and liquidity backdrop is still supportive, though the monetary easing cycle is at a mature stage. In mainland China, monetary policy is expected to remain moderately loose, supporting growth and price recovery. The People’s Bank of China (PBoC) has also pledged to promote high-level financial opening-up and RMB internationalisation, which are positive for RMB bonds. In India, with inflation expected to be at or below the target for an extended period, the Reserve Bank of India (RBI) may be positioned for a prolonged pause in its interest rate moves. Although Bloomberg’s decision on the potential inclusion of India government bonds in its global aggregate index has been deferred to mid-2026, the continued eligibility review means that a positive medium-term tailwind remains in place.

Overall, Asian currencies have been undervalued on a Real Effective Exchange Rate (REER) basis over the past few decades. Asia currencies may be driven by risk sentiment, AI flows, stronger external positions and tech supply chain realignment.

This document provides a high level overview of the recent economic environment. It is for marketing purposes and does not constitute investment research, investment advice nor a recommendation to any reader of this content to buy or sell investments. This content has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination The views expressed were held at the time of preparation; are subject to change without notice and may not reflect the views expressed in other HSBC Group communications or strategies. You should be aware that the value of any investment can go down as well as up and investors may not get back the amount originally invested. Furthermore, any investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in established markets. Any performance information shown refers to the past and should not be seen as an indication of future returns. You should always consider seeking professional advice when thinking about undertaking any form of investment. This communication has not been reviewed by the Securities and Futures Commission.

Source: Bloomberg, HSBC Asset Management, March 2026.

Note 1: Source is Bloomberg, MSCI, as of 31 January 2026. MSCI country indices are used to represent the equity performance of the indicated markets.

Note 2: Based on MSCI India Index vs MSCI Emerging Markets Index. Source is MSCI, Goldman Sachs, January 2026.

Note 3: Source is Datastream, MSCI, Morgan Stanley Research, January 2026.

Note 4: Source is JPMorgan, January 2026 report.

Note 5: Source is JPMorgan, December 2025 report.

Past performance does not predict future returns. Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecasts, projections or targets. The views expressed above were held at the time of preparation and are subject to change without notice. The information provided does not constitute any investment recommendation or advice. Diversification does not ensure a profit or protect against loss. This information should not be construed as a recommendation to invest in the specific country, product, strategy or sector. For illustrative purposes only.

Important information

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. Past performance contained in this document is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in Emerging Markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Mutual fund investments are subject to market risks, read all scheme related documents carefully.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Global Asset Management Global Investment Strategy Unit at the time of preparation, and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Global Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity.

We accept no responsibility for the accuracy and/or completeness of any third party information obtained from sources we believe to be reliable but which have not been independently verified.

Investment involves risk. Past performance is not indicative of future performance. Please refer to the offering document for further details including the risk factors. This document has not been reviewed by the Securities and Futures Commission.

HSBC Global Asset Management is the brand name for the asset management business of HSBC Group. The above communication is distributed in Hong Kong by HSBC Global Asset Management (Hong Kong) Limited.

Copyright © HSBC Global Asset Management (Hong Kong) Limited 2026. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Global Asset Management (Hong Kong) Limited.

Content ID: D067865_v1.0; Expiry Date: 31.03.2027