Fixed Income Insights

In a nutshell

What is the credit impact of AI-driven power demand?

- AI and data centres are becoming major drivers of global electricity demand, prompting large-scale investment in generation, grids, and storage, with the US alone expected to see about USD 30 billion per year of AI-related power capex and significant associated debt issuance – on top of increased debt issuance from hyperscalers

- Credit impacts are most pronounced in the US, where rising AI-related electricity and natural-gas demand supports utilities, independent power producers, and midstream energy, but also introduces project-finance, counterparty, regulatory, and affordability risks, especially as off-grid and hybrid solutions proliferate

- In Asia, China appears structurally well-positioned to absorb AI demand within an already strong, policy-supported system, while Japan and India face larger incremental investment needs, with potential credit upside for utilities that successfully expand low-carbon capacity

- In Europe, AI-related demand is currently a small part of a broader electricity “investment supercycle”, with grid modernisation and renewables integration driving issuance; utilities are generally able to manage balance-sheet pressure, though political and regulatory risks around affordability might emerge

What is the credit impact of AI-driven power demand?

AI is rapidly driving up global electricity demand, requiring major capital investment and grid upgrades. With annual capex of USD30 billion projected over the next five years to support AI-related power infrastructure in the US alone, data centres are expected to drive significant levels of debt issuance.

AI requires major capital investment in electricity generation infrastructure. Renewables and storage will meet much of this need, while regional risks and technology advances will shape future supply and financial exposure.

Artificial intelligence is becoming a meaningful additional driver of electricity demand, adding to longer-running trends linked to electrification of the economy. Supporting this shift will require substantial capital, with expectations of increased debt issuance across regions and a particularly large concentration in the United States.

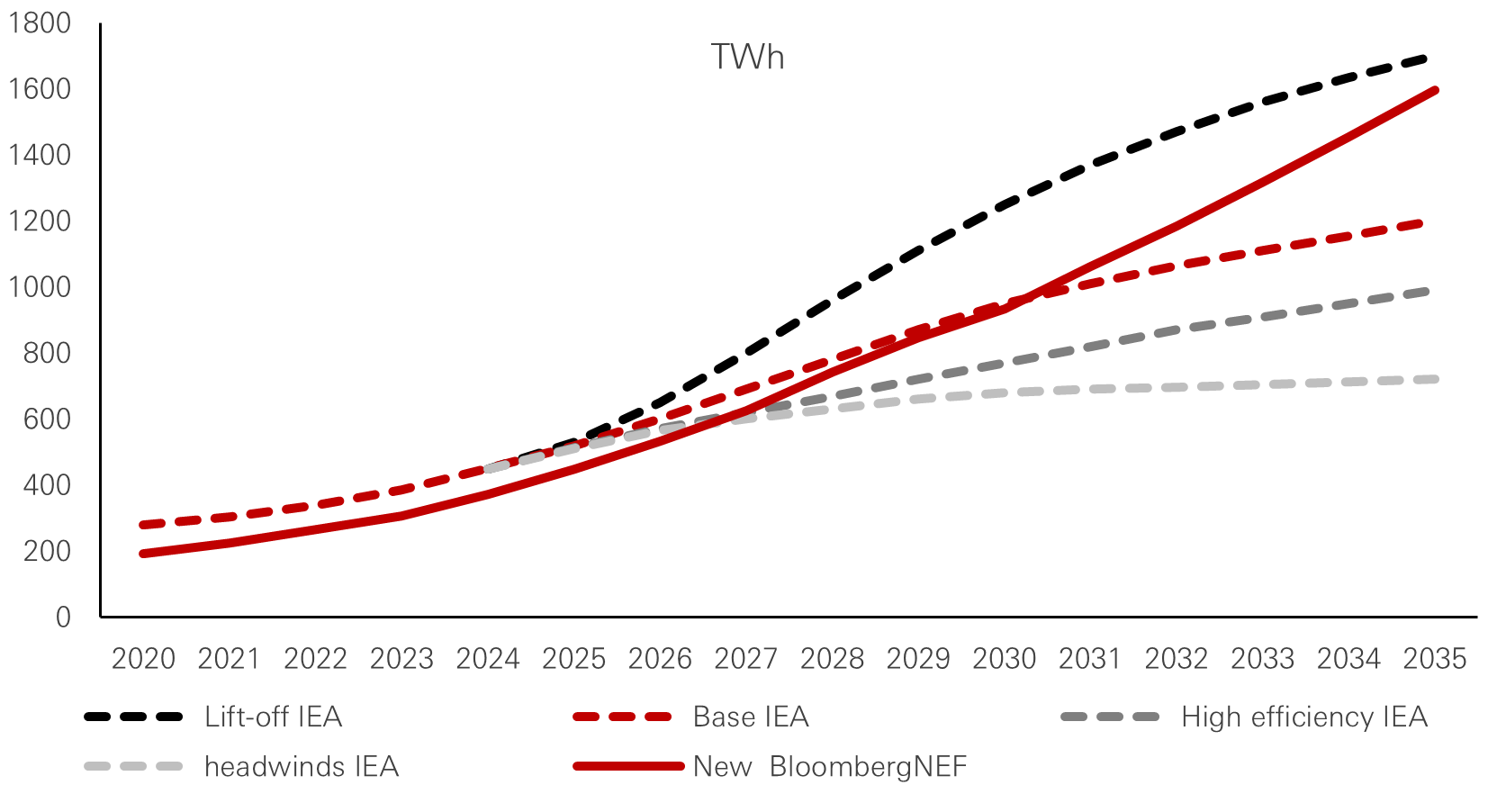

Forecasts for AI-related electricity demand continue to rise. Recent projections from Bloomberg show materially higher estimates than the International Energy Agency’s updated figures from six months earlier, especially for post-2030. Although uncertainty remains high, the direction of travel points upward. Scenario ranges reflect differing assumptions about efficiency improvements and cooling systems. Air cooling still accounts for more than 20 per cent of data-centre electricity consumption, but potential gains from liquid cooling should be realised. Even so, base-case assumptions have moved away from the more pessimistic projections.

Figure 1: AI adoption has accelerated

Click the image to enlarge

Source: IEA, Bloomberg, HSBC Asset Management, December 2025.

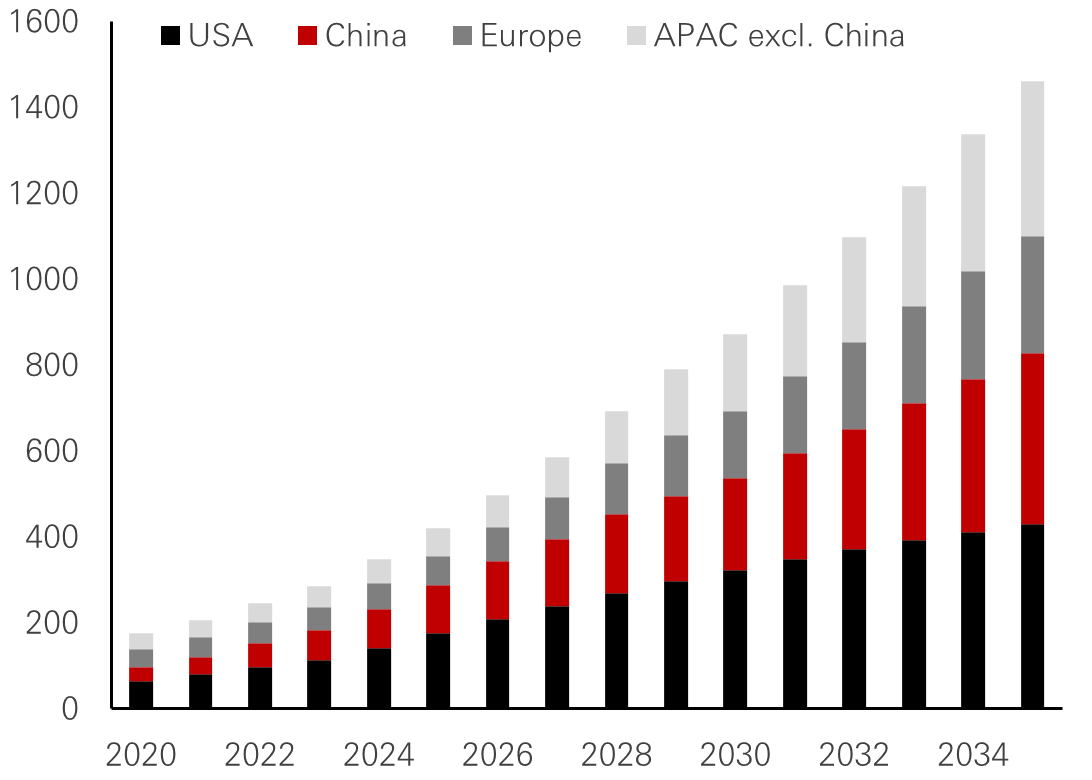

AI’s contribution to incremental electricity demand will vary widely by region. Globally, AI may represent around 10 per cent of future growth, but in emerging markets the contribution is closer to 5 per cent, given other dominant drivers such as industrialisation. In the United States, AI and data centres could account for more than half of incremental demand. The concentration of growth is significant: China and the US together represent over 80 per cent of expected data-centre electricity expansion to 2030. China benefits from higher reserve margins – the extra generating capacity available over and above the expected peak electricity demand – while US and Europe face ageing networks and affordability challenges. Delays in building new generation capacities and/or in modernising and extending the electric grid could be a major headwind for the development of AI/DC.

Renewables and storage are expected to meet roughly half of additional global data-centre load, supported by existing electricity grids. Renewables have shorter lead times compared with alternatives, while dispatchable gas is expected to complement the system in the US and coal may continue in some emerging markets. New technologies such as geothermal, carbon capture and storage, utility-scale batteries and small modular reactors are also emerging as potential contributors to future supply. For utilities, counterparty exposure is the primary risk for generation assets should the credit quality of technology companies weaken. Network investments embedded in regulated asset bases remain supported by existing customers, limiting financial risk.

Figure 2: AI-driven power demand (terawatt-hours)

Click the image to enlarge

Source: Bloomberg, HSBC Asset Management, December 2025

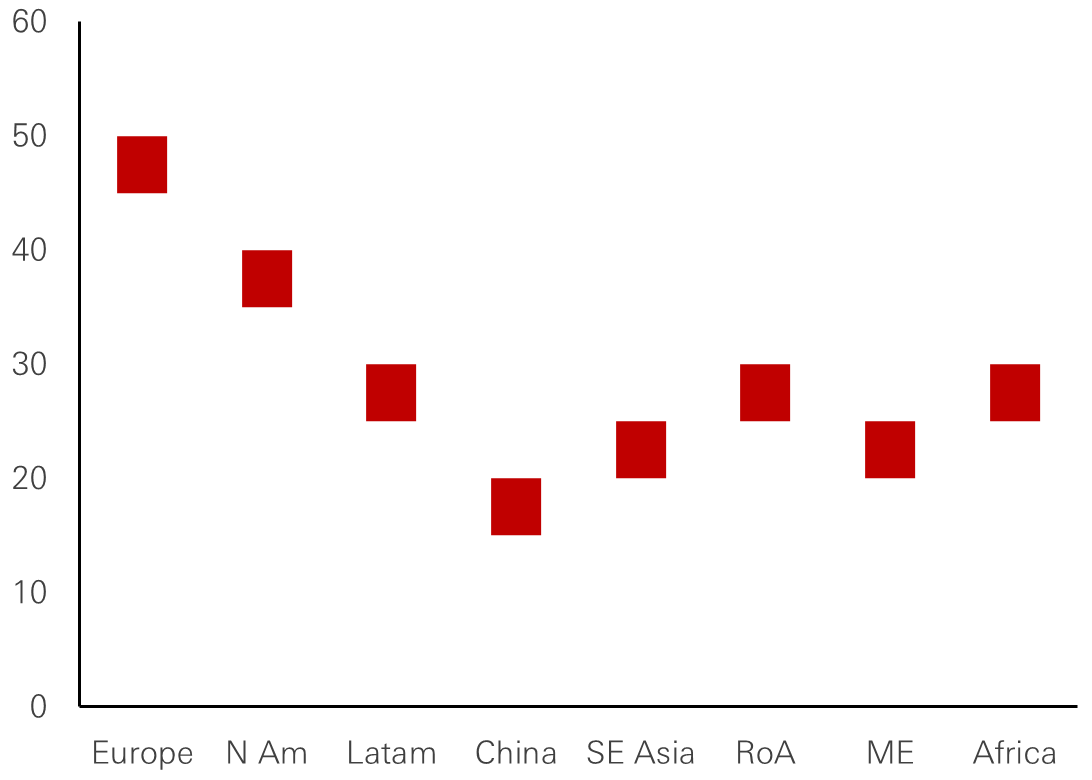

Figure 3: Average cable age (years)

Click the image to enlarge

Source: Nexans, HSBC Asset Management, December 2025

Figure 4: Reserve margin (per cent)

Click the image to enlarge

Source: BofA, Korea Power Exchange, HSBC Asset Management, December 2025

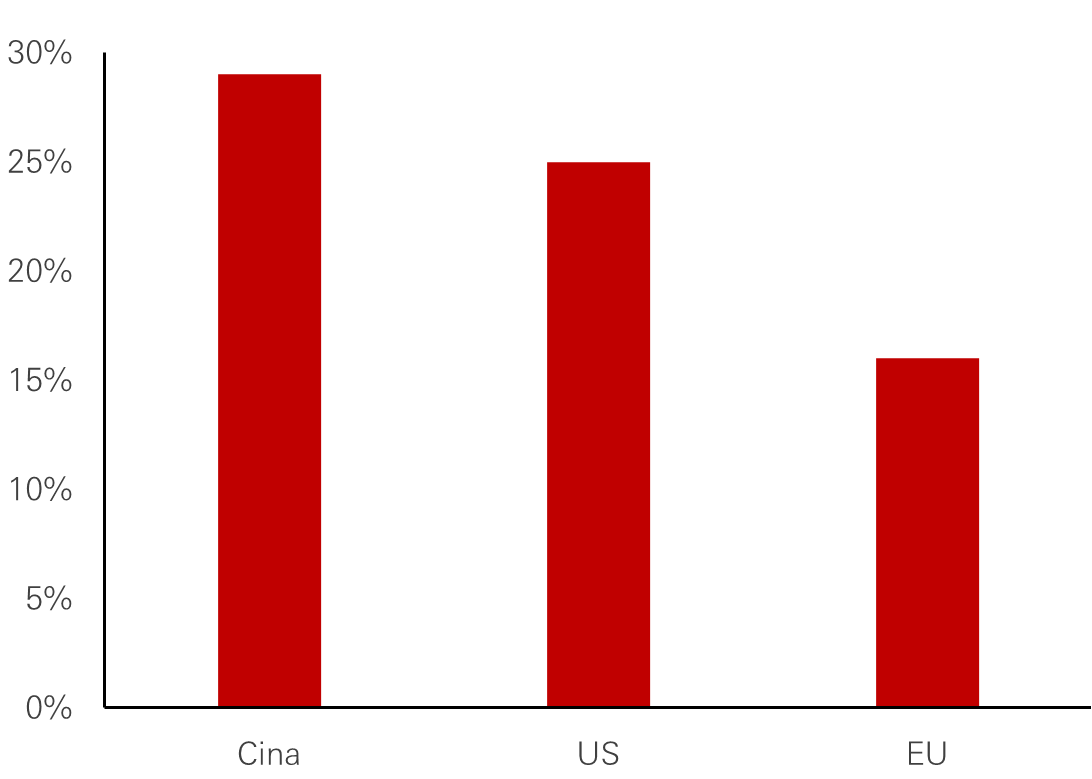

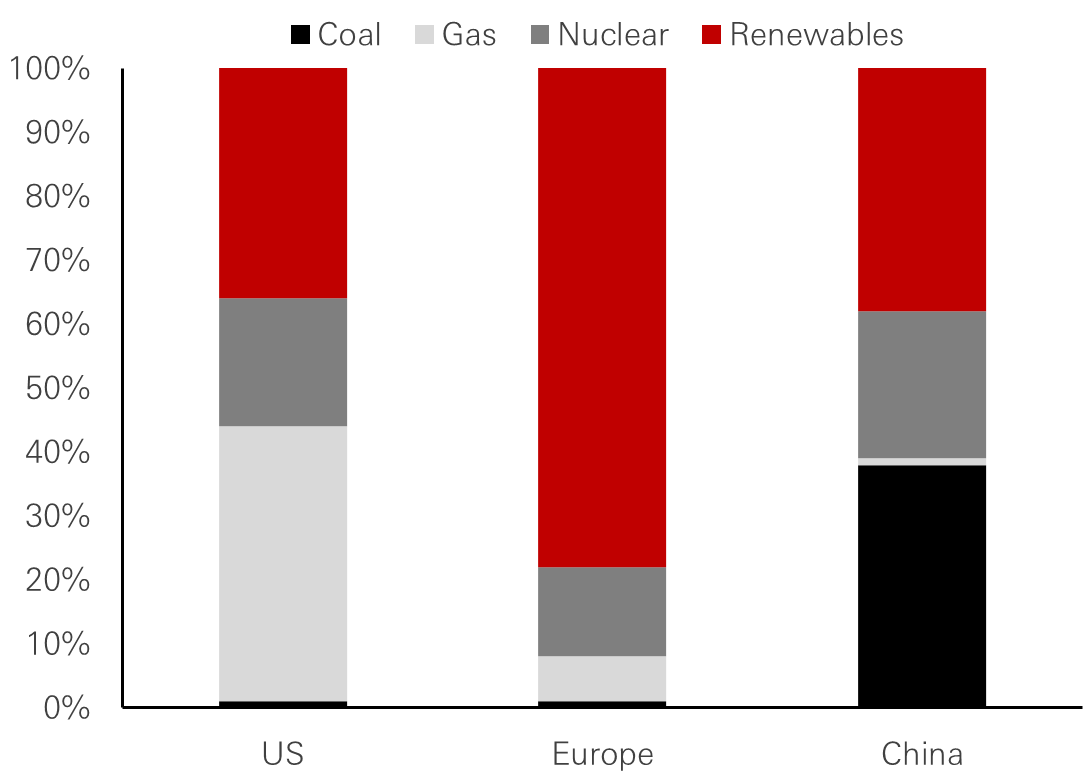

Figure 5: Electricity mix for data centres in 2035

Click the image to enlarge

Source: IEA, HSBC Asset Management, December 2025

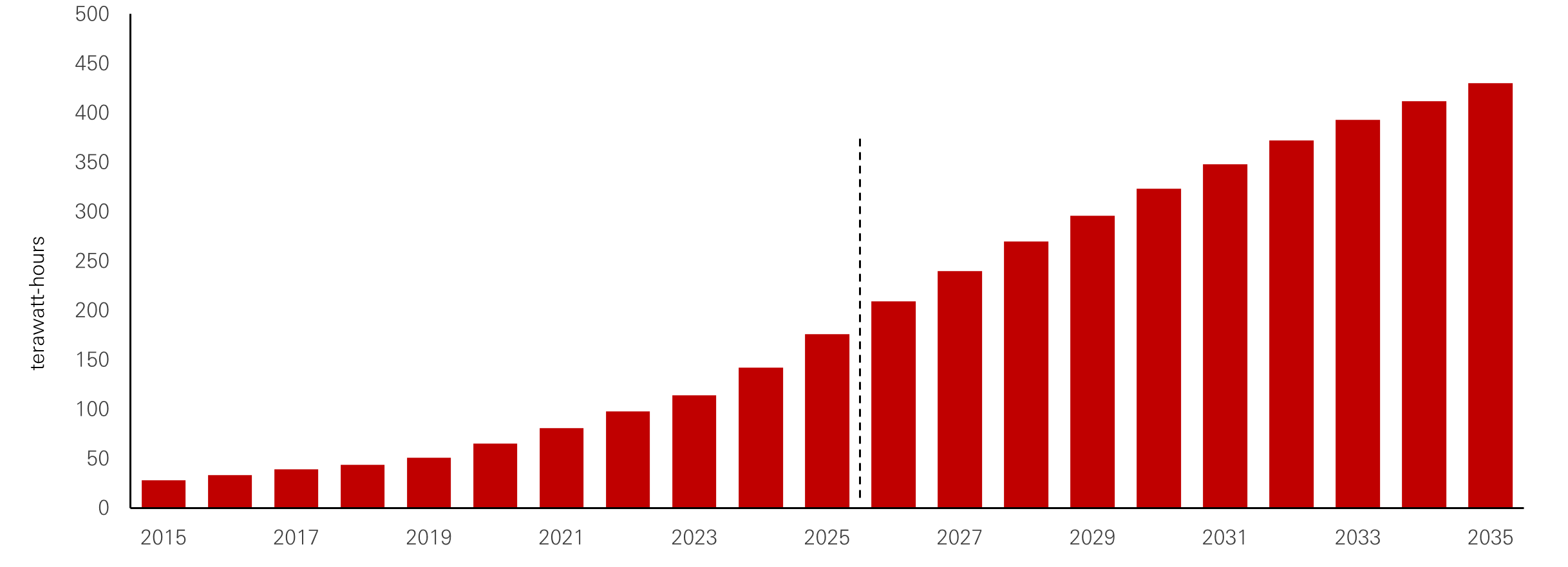

AI data centres are driving a surge in US electricity and natural gas demand, with USD30 billion likely invested annually in infrastructure. Financing is shifting toward off-balance-sheet and project-specific deals. Utilities face time, cost, affordability and reliability challenges, prompting hyperscalers to increasingly adopt off-grid power.

The United States leads the global surge in AI-driven electricity demand, with data centres accounting for a significant share of new power requirements. Over the next five years, an estimated USD30 billion annually will be spent on capital expenditures to support AI-related power infrastructure – excluding additional investments by midstream and upstream energy providers.

Figure 6: US power demand from AI data centers to triple in 10 years

Click the image to enlarge

Source: HSBC Asset Management, BNEF,EEI, December 2025. NB: the figures are before the Q3 earnings call for the hyperscalers excluding ORCL

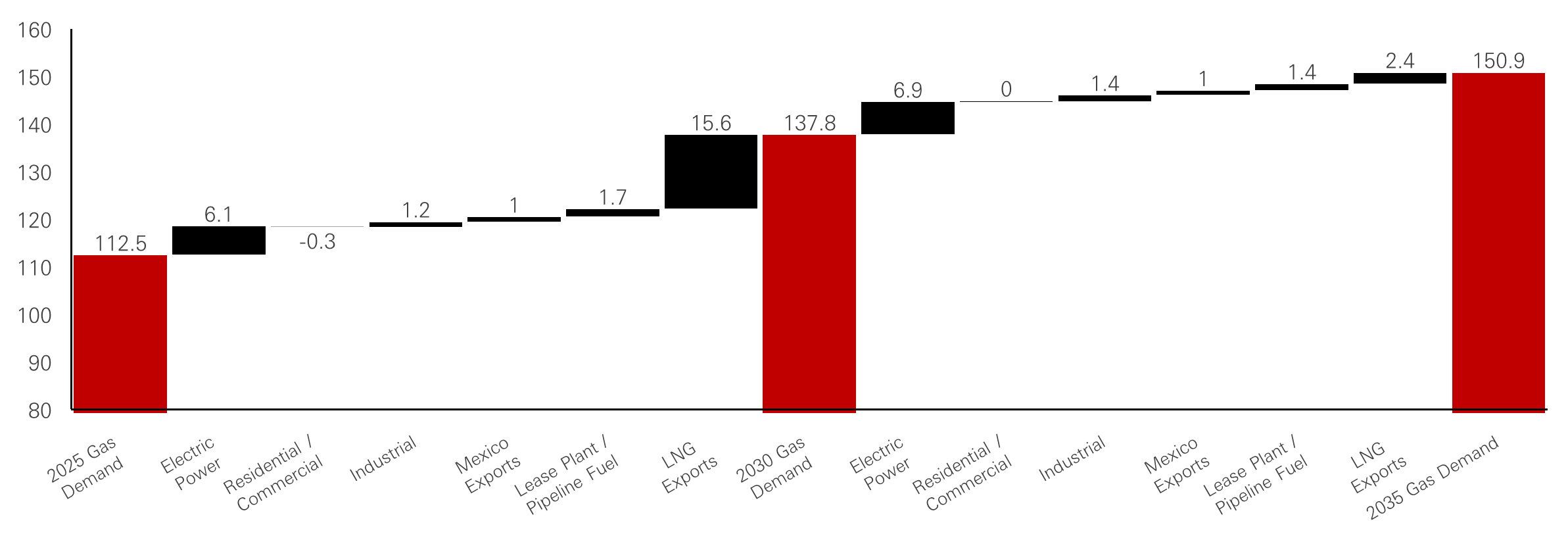

Natural gas has become pivotal in addressing these demands due to its reliability and ability to provide uninterrupted electricity, a critical requirement for data centres that operate continuously. By 2030, AI-related data centres are projected to account for up to 40 per cent of incremental US natural-gas demand for power generation, with estimates ranging from 2.5 billion to 6 billion cubic feet per day. This dynamic not only supports the credit profiles of natural gas producers and midstream companies but also drives demand for energy infrastructure bonds. However, AI is not the primary driver of US natural-gas demand, as LNG exports remain the dominant factor. Across all drivers, cumulative US natural-gas demand is expected to increase by roughly 30 per cent through 2025.

Figure 7: 2025-35 gas demand changes (Bcf/d)

Click the image to enlarge

Source: HSBC Asset Management, Morgan Stanley, EIA, S&P Global, December 2025.

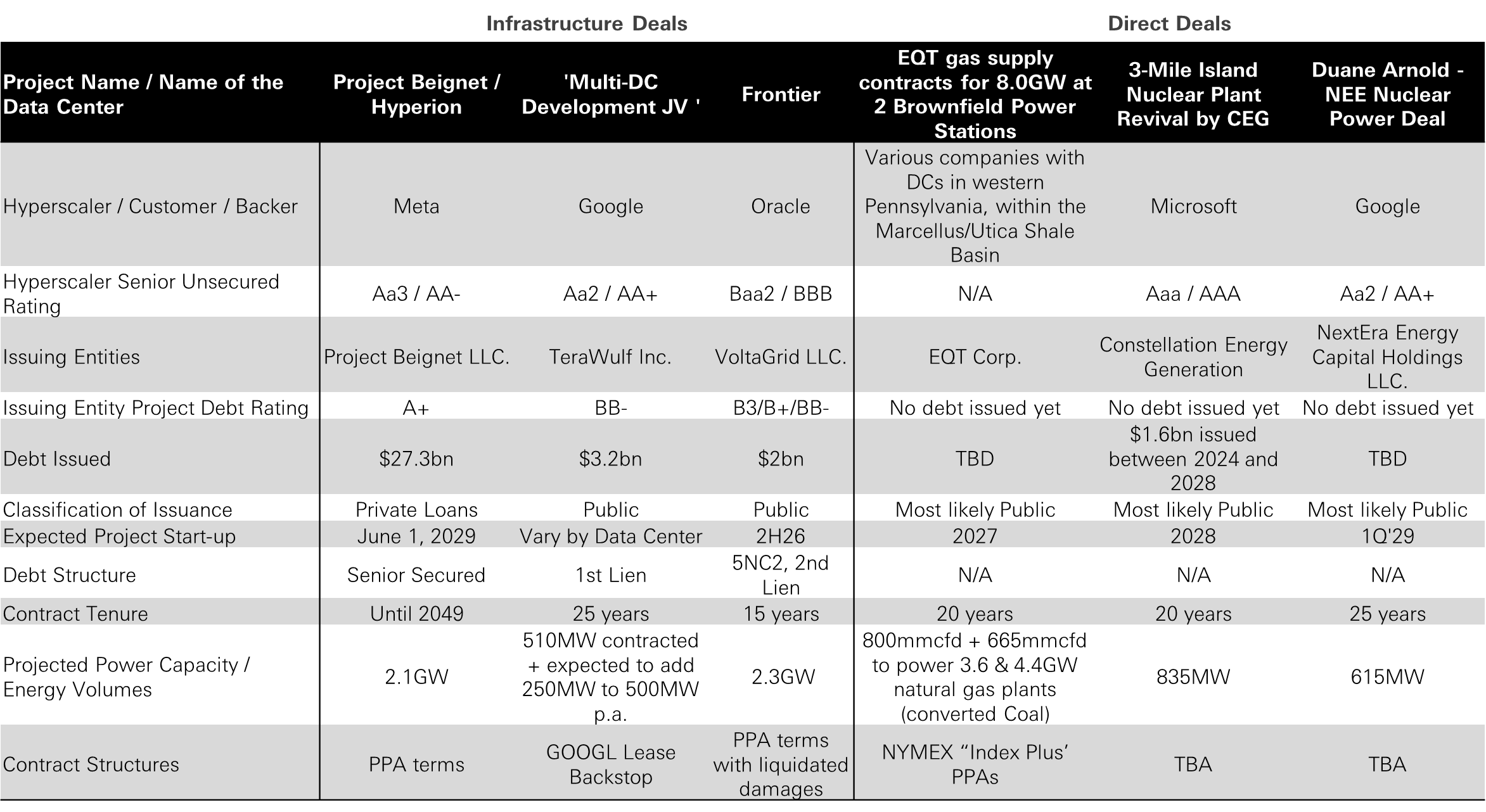

The urgency of AI deployment has made "time-to-power" a critical constraint for hyperscalers, alongside cost and reliability. A survey of data-centre developers highlights utilities as the key bottleneck to expansion, with time, cost, and reliability emerging as the most significant challenges. These constraints have led to the adoption of diverse infrastructure solutions, including grid-connected, hybrid, and off-grid systems. For example, Oracle’s off-grid development near the Permian Basin relies on distributed natural-gas engines as its primary power source. Google’s joint venture is structured to support close to one gigawatt of demand, while Meta’s two-gigawatt Hyperion facility combines grid connections with new natural-gas-based combined-cycle plants built specifically for the site under long-term arrangements. Nuclear assets should increase within the overall mix, with previously retired plants expected to restart under long-term power-purchase agreements.

Financing structures are evolving to meet these demands, with off-balance-sheet and project-specific agreements becoming more prevalent. Upstream energy producers have partnered with hyperscalers to supply natural gas directly to repurposed brownfield sites, such as retired coal plants converted into natural-gas generation. Large energy companies and hyperscalers have outlined multi-gigawatt development plans, many scheduled for completion before 2027, reflecting the rapid evolution of the infrastructure landscape.

Figure 8: Infrastructure deals

Click the image to enlarge

Source: HSBC Asset Management, Company Filings, December 2025.

Affordability concerns are emerging as a growing challenge, particularly for regulated utilities and on-grid solutions. In regions such as the Northeast, Mid-Atlantic, parts of the Midwest, and California, increases in customer bills have been driven largely by grid-investment requirements rather than underlying demand. Hyperscalers have responded by avoiding jurisdictions facing grid congestion or complex regulation, instead turning to off-grid or hybrid systems. Discussions around potential policy responses, including separate tariff structures for large industrial users like data centres, are becoming more common. However, it remains unclear how regulators will address these affordability challenges while ensuring sector stability.

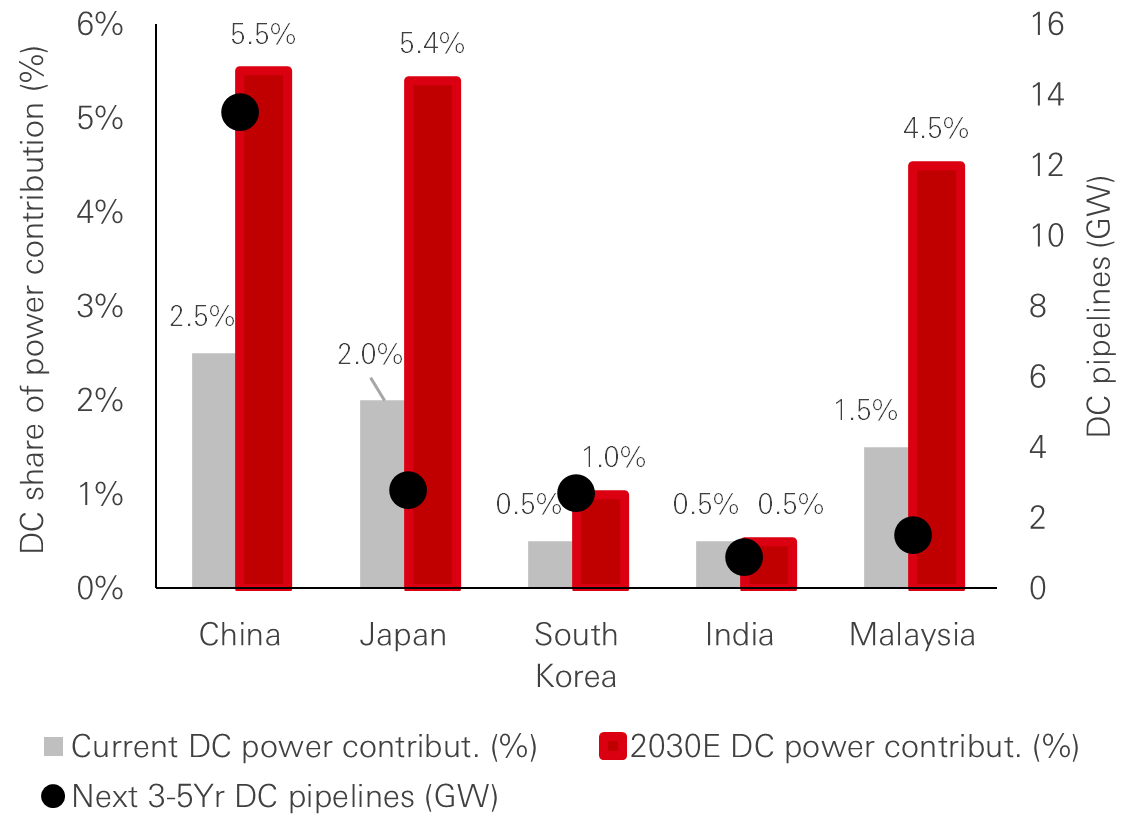

AI-driven electricity demand is reshaping Asia’s power landscape, with China well-positioned due to strong infrastructure and policy support, Japan facing the largest growth impact, and India and Southeast Asia requiring major investments and low-carbon capacity to meet future needs.

Across Asia, the effects of AI-driven electricity demand vary significantly by country. China is emerging as a key player due to its larger capacity base and structural advantages. AI-driven electricity demand contributes a moderate 12 per cent to domestic electricity-demand growth. This is manageable within the broader context of the country's focus on energy security and industrial expansion. China's power system benefits from high electricity reserve margin and upgraded grid infrastructure, enabling it to integrate new AI-related loads without immediate stress on the system. Policy initiatives – such as the “East Data, West Computing” programme, which allocates data storage and power generation to the capacity rich western regions to support application usage in the highly developed areas around the east coast – are pivotal in managing demand. By directing data-centre activity towards regions with surplus renewable power, these measures help to balance rising electricity needs while minimising reliance on new fossil-fuel generation. This approach aligns with China's net-zero commitments, with low-carbon power capacity expected to increase by 85 per cent over the next five years. These structural and policy-driven factors make China better powered up for AI.

In contrast, Japan is poised to experience the most pronounced effects of AI-related electricity demand within Asia. AI-driven data centres are projected to account for over 60 per cent of Japan’s future power-demand growth, marking a significant shift for a utility sector that has faced declining demand over the past decade. The anticipated 5 per cent increase in power demand over the next ten years could stabilise the credit outlook for Japanese utilities, particularly those with greater exposure to low-carbon power generation.

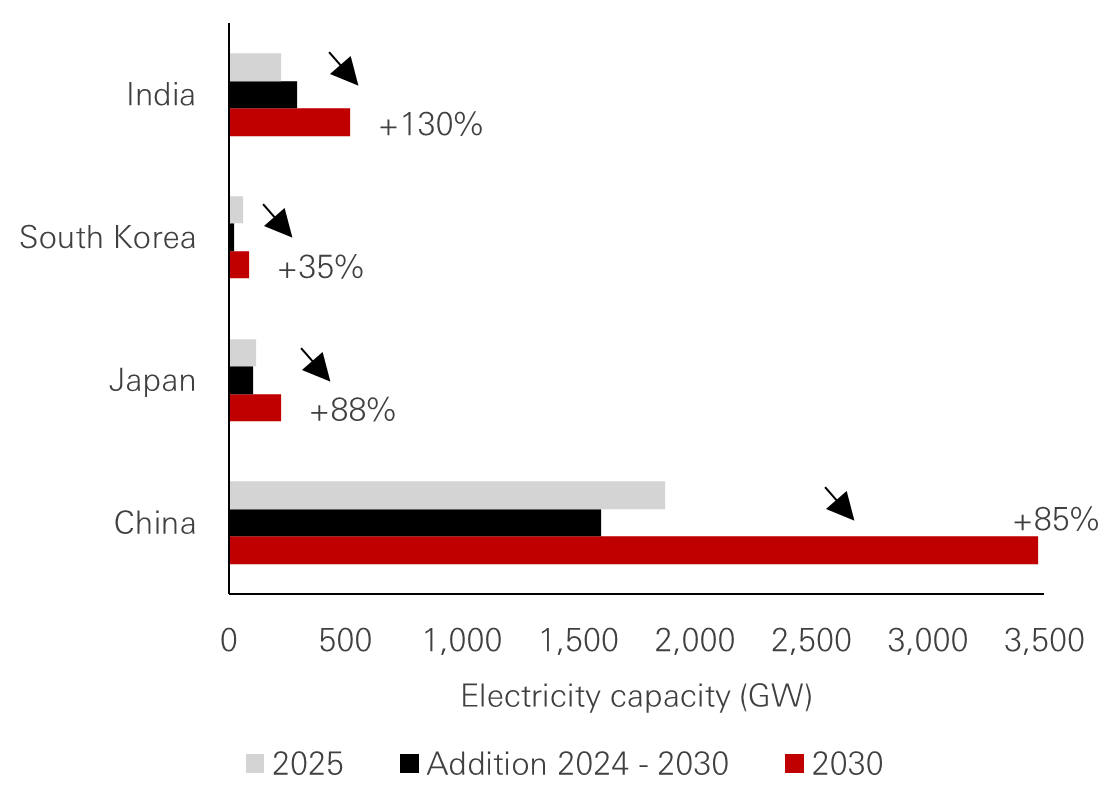

In South Korea, AI-driven electricity demand is expected to account for around 15 per cent of future electricity-demand growth, reflecting the continued influence of high-end manufacturing and electric-vehicle charging. In Southeast Asia and India, AI-linked demand remains limited based on the current pipeline. However, both Japan and India face significant investment needs to avoid delays in their pipelines. India, for instance, requires more than 12 gigawatts of new generation capacity and substantial grid upgrades. Across Asia, utilities remain influenced by national energy-security and industrial-expansion goals, alongside the need for a significant increase in low-carbon capacity. India and China are expected to require more than 80 per cent to 130 per cent growth in low-carbon generation over the next five years to meet these objectives.

Overall, the impact on the balance sheets of Asian utilities should be manageable. Japan and India stand out in needing to increase capex to avoid falling behind in the AI race, although in Japan, as much as it is a mitigant to otherwise falling demand, we see it as credit positive.

Figure 9: DC share of power demand to increase

Click the image to enlarge

Source: Company disclosure, Barclays, Cushman & Wakefield, UBS, Morgan Stanely, Moody’s HSBC GAM est, November 2025.

Figure 10: Asia lower carbon power (solar + wind + nuclear) investment plan by 2030

Click the image to enlarge

Source: HSBC Asset Management, UBS, BOFA, company disclosure, November 2025.

Emerging Markets ex. Asia: Neutral credit impact with sustainability upside.

In emerging markets such as Latin America, the Middle East, and Africa, the credit impact of AI-driven power demand is expected to be neutral. These regions account for a small share of global data-centre infrastructure, and their existing reserve margins are sufficient to accommodate additional demand. Latin America, in particular, is well-positioned to meet new power requirements with its abundant renewable energy resources. Similarly, utilities in the Middle East and Africa have incorporated AI-related demand into their long-term planning, minimising the need for additional capital expenditures.

Europe: Limited credit impact amid broader grid modernisation.

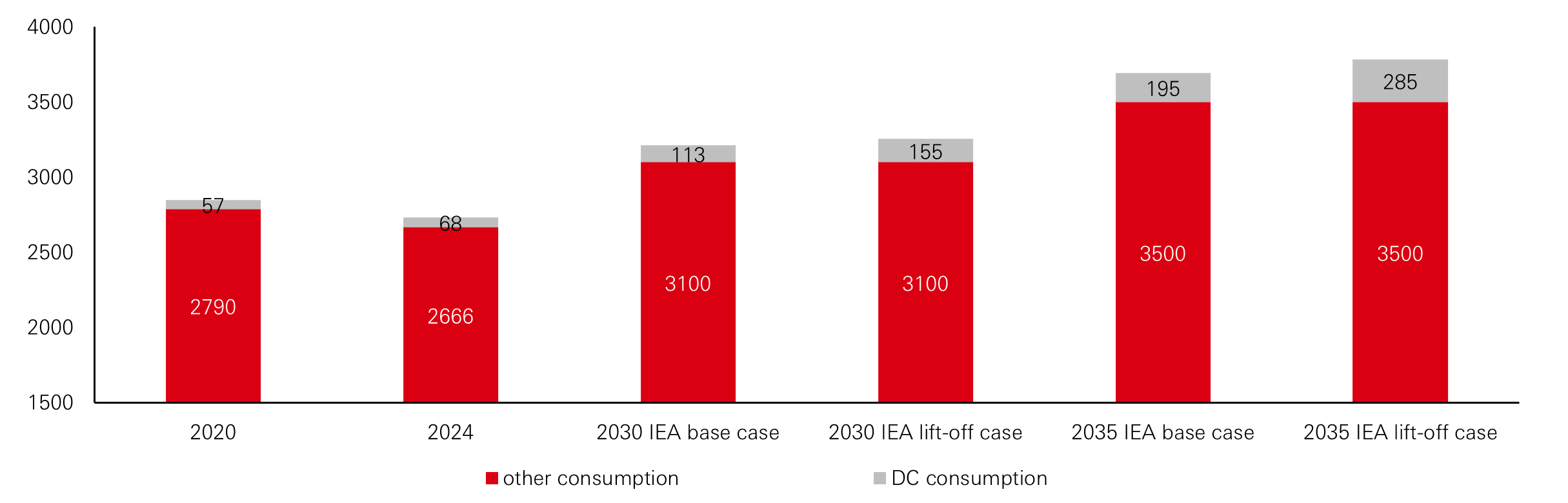

In Europe, the credit impact of AI-driven power demand is expected to be minimal, at least in the short term, in the broader context of an ‘investment supercycle’ which is already reshaping credit dynamics as Europe revamps its electricity system. Data centres account for a low single-digit percentage of total electricity demand growth, and the region's utilities are primarily focused on modernising grids and integrating renewable energy.

This investment is being financed through capital markets, with more than USD20 billion in capital raised recently and an additional USD10 billion expected in the coming months. While affordability concerns could emerge as a political risk, particularly in regions with high electricity prices and capacity constraints, regulatory reforms and targeted tariffs for large industrial users may mitigate these risks. European utilities are well-positioned to manage the financial demands of grid upgrades without significant pressure on their balance sheets.

Would the electricity demand from Data Centers accelerate in couple of years, the European electric system may be in a better position to cope with it. We expect a smarter electric grid to better integrate intermittent renewables helped by the strong development of utility-scale batteries. This would improve the European reserve margin as less back-up capacities for renewables would be needed, and more capacities would be available at peak time.

Figure 11: European electricity consumption in TWh (IEA, announced pledges scenario)

Click the image to enlarge

Source: HSBC Asset Management, IEA, November 2025.

We still expect high issuance from European utilities to finance the investment supercycle. We also believe that US utilities will come more and more to the EUR market, in particular with hybrid bonds that will enable them to benefit from the equity content of such subordinated notes to finance their increased capex programme (ex NextEra hybrid issuance at the end of 2025). Since corporate hybrids bonds have a long-standing history in Europe and are an important part of the market, EUR investors are more sophisticated when it comes to this market segment that presents opportunities for both issuers and investors.

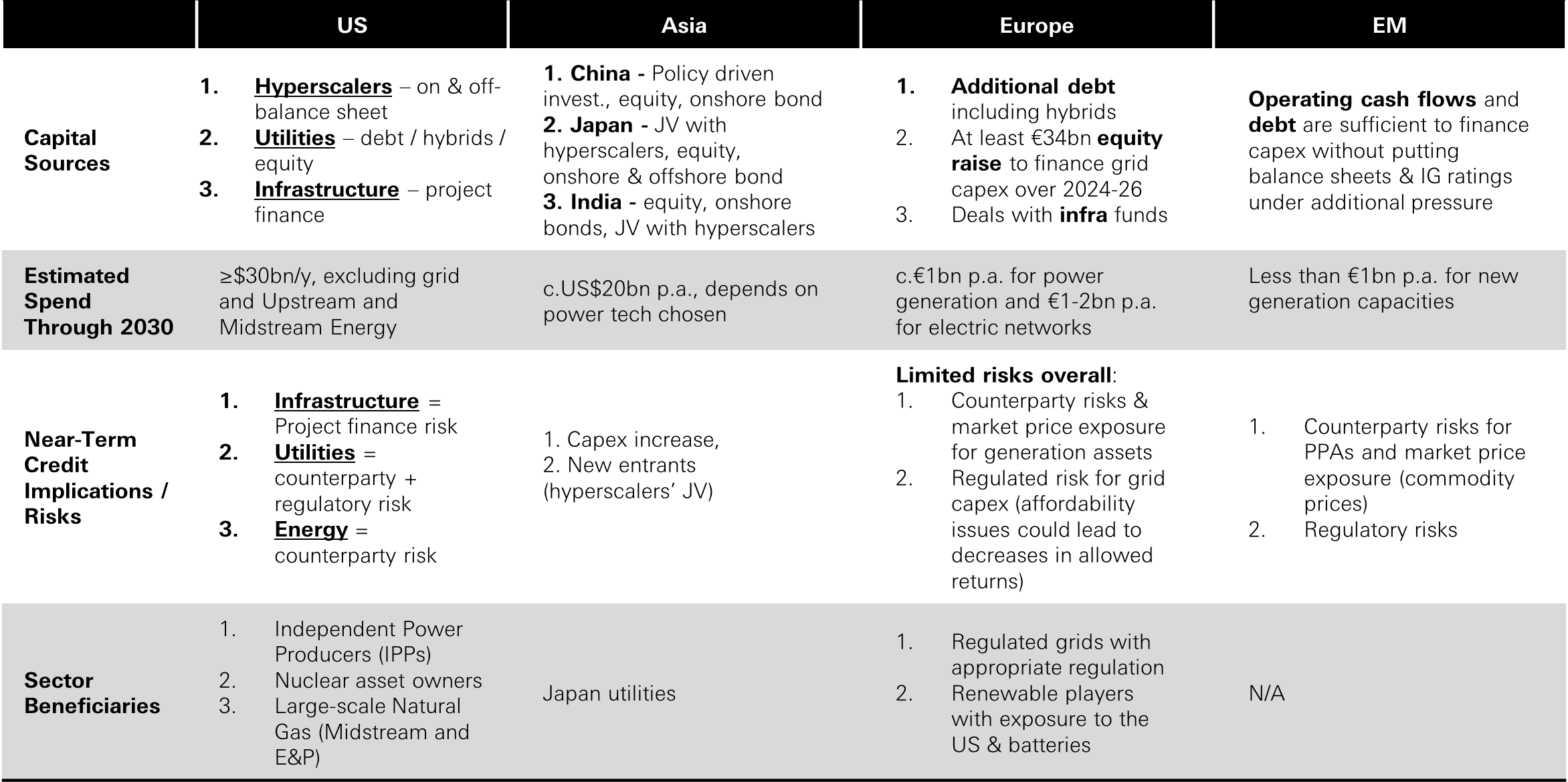

Credit implications from AI-driven power demand for sectors and geographies

Click the image to enlarge

Source: HSBC AM, January 2026.

Source: HSBC Asset Management, February 2026. The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security.