Fixed Income Insights

In a nutshell

What are the macro impacts of the AI investment boom, and does history indicate the risk of a future bust?

- The US AI investment boom is materially lifting GDP growth, driven by large-scale data-centre and AI-related capex that could raise the US investment-to-GDP ratio by around 1.5–2 percentage points by 2028

- The cycle resembles the late-1990s dotcom boom in scale and duration, but investment gains remain highly concentrated in tech, with limited spillover so far to broader non-tech capital spending

- The AI build-out is capital-intensive, generating limited direct job creation and uneven wealth effects, with benefits skewed towards higher-income households via equity markets rather than broad-based labour-market gains

- Generative AI adoption is exceptionally rapid, but aggregate productivity gains remain uncertain and may be delayed by organisational, skills, and governance frictions that slow diffusion beyond early adopters

- For fixed income markets, AI-driven capex supports US growth and reduces the likelihood of aggressive rate cuts, while creating more differentiated credit risks between AI-linked issuers and sectors more exposed to higher-for-longer interest rates

What are the macro impacts of the AI investment boom, and does history indicate the risk of a future bust?

The AI investment boom is driving GDP growth, mainly through hyperscaler capex, but its economic benefits in the short term are concentrated and capital-intensive, with limited job creation and uneven wealth effects.

The recent investment surge has obvious parallels to the late-1990s dotcom boom, rapidly boosting US growth. But gains remain concentrated in tech sectors, with limited spillover to broader investment so far.

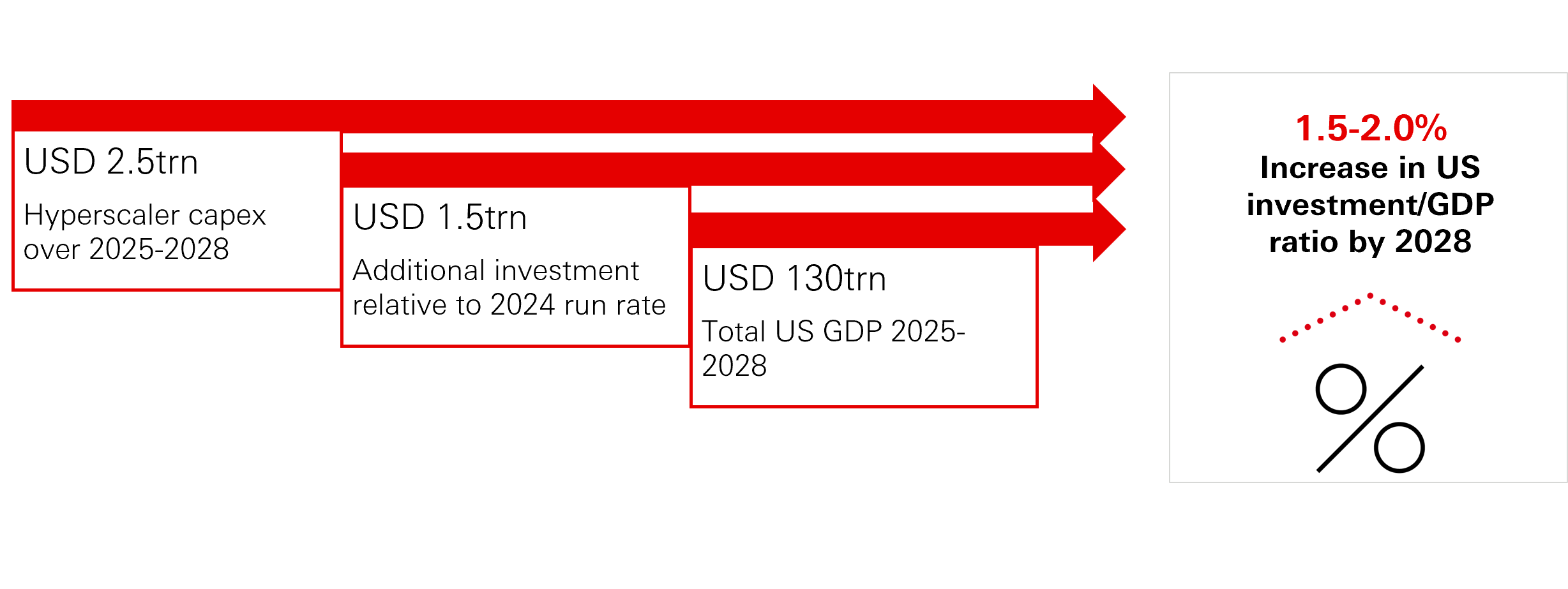

The AI investment boom has become a key pillar of US growth. Hyperscalers have repeatedly revised capital-expenditure plans higher, with cumulative data-centre and AI-related capex for 2025-2028 now estimated at around USD 2.5 trillion. Adjusting for the already elevated 2024 run-rate brings the incremental figure closer to USD 1.5 trillion. Set against an estimated USD 130 trillion in cumulative US GDP over the same period, this implies an increase in the investment-to-GDP ratio of roughly 1.5-2 percentage points by 2028.

In growth terms, the effect is already visible. In the first half of the 2025, US GDP grew by about 1.5 per cent, with roughly one percentage point attributable to AI-related investment. Given headwinds from tariffs and still-restrictive interest rates, without the AI investment boom, growth could have fallen below 1 per cent, a level historically associated with the risk of economy lapsing into recession.

Figure 1: US investment/GDP ratio by 2028

Click the image to enlarge

Source: Morgan Stanley, Macrobond, HSBC AM, December 2025.

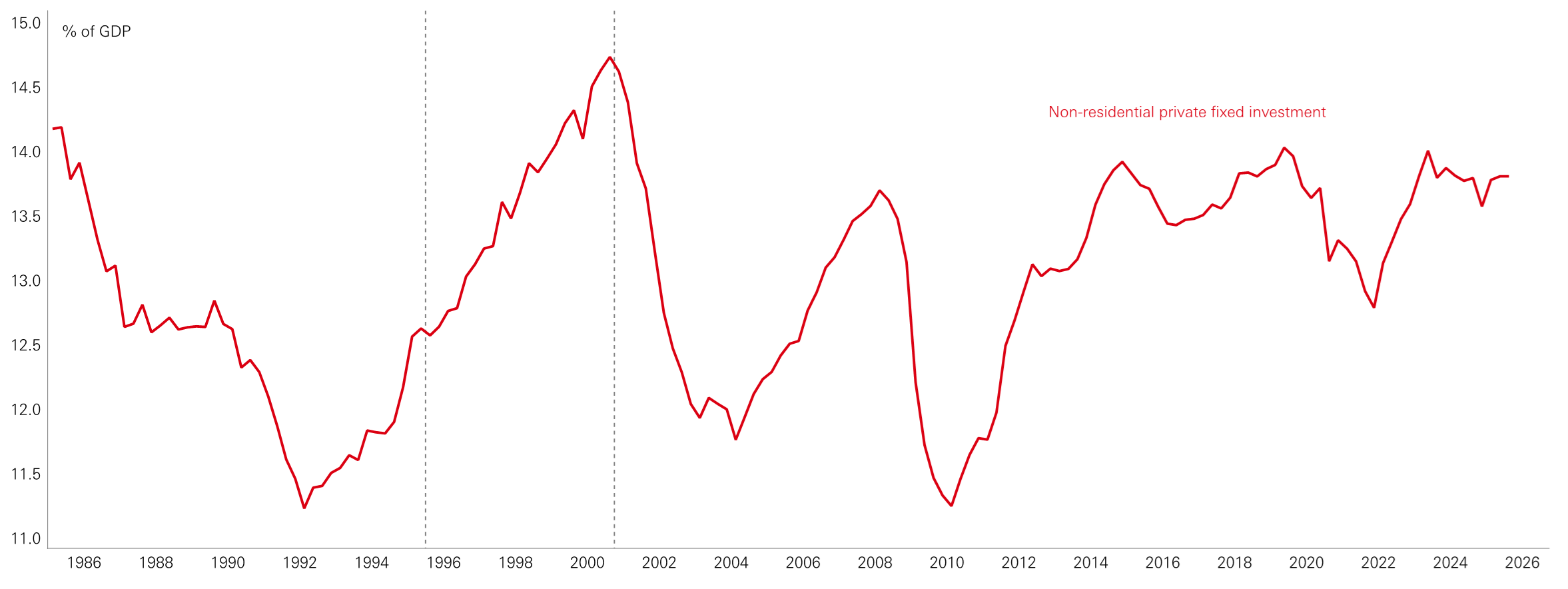

The late-1990s dotcom period provides a potentially useful historical precedent for today’s AI investment cycle. Then, a multi-year investment surge lifted the investment-to-GDP ratio by approximately 2 per cent, following a period of subdued capex. The present cycle appears similar in scale, although the early phase has unfolded faster. History suggests that such booms tend to run for several years rather than one or two, and that they often end with some degree of retrenchment once overcapacity becomes apparent. At this stage, however, available data point to an ongoing boom rather than an imminent reversal.

Figure 2: Dotcom investment boom lasted five years

Click the image to enlarge

Source: Macrobond, HSBC AM, January 2026.

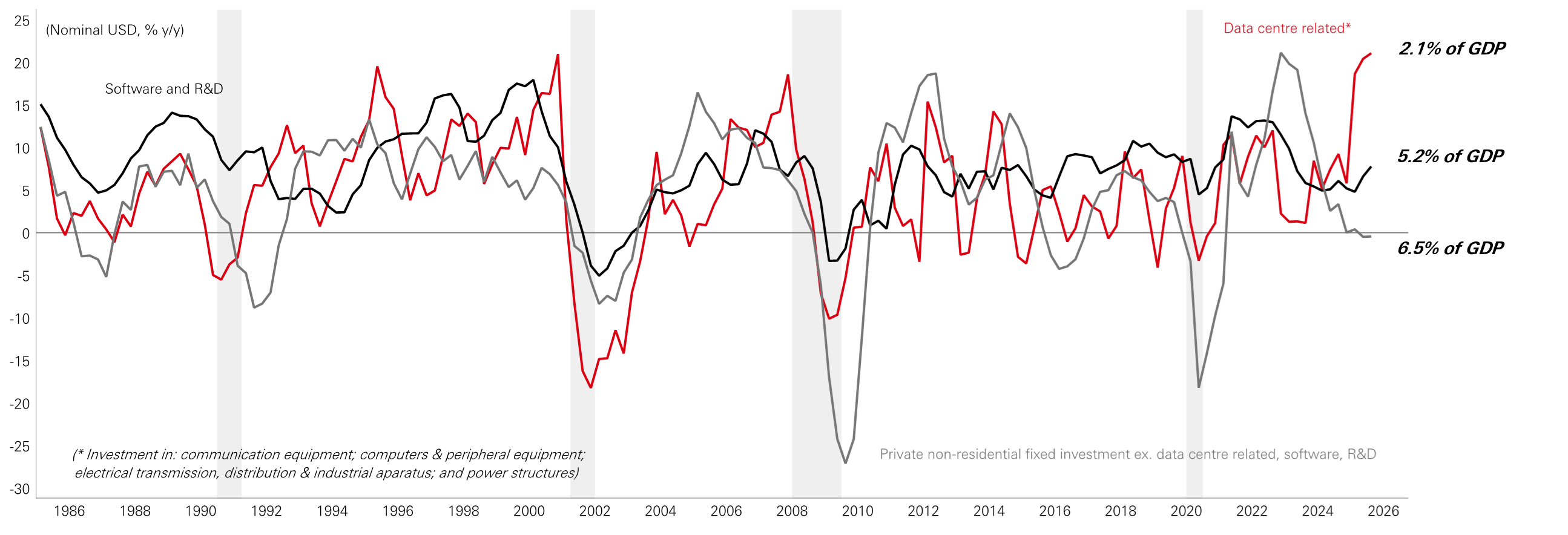

Despite data-centre-related spending accounting for roughly 2.0 per cent of GDP and growing rapidly, non-tech fixed investment is closer to 6.5 per cent of GDP and has shown essentially zero growth over the last year. This underlines how concentrated the upswing has been and the lack so far of a ‘crowding in’. Our central case is that strong AI capex and steady software and R&D spending coincide with only a modest recovery in other forms of investment. An upside scenario would see AI act as a catalyst for a broader strong investment upswing. One downside risk is that sustained AI capex contributes to higher-for-longer interest rates, raising the cost of capital for more interest-sensitive sectors and limiting investment elsewhere.

Figure 3: Divergent investment trends

Click the image to enlarge

Source: Macrobond, HSBC AM, January 2026.

The AI investment boom is failing to drive significant direct job growth and mainly benefiting higher-income households through equity market gains. Future growth depends on sustained profits, and any disappointment could quickly impact investment, employment, and consumption.

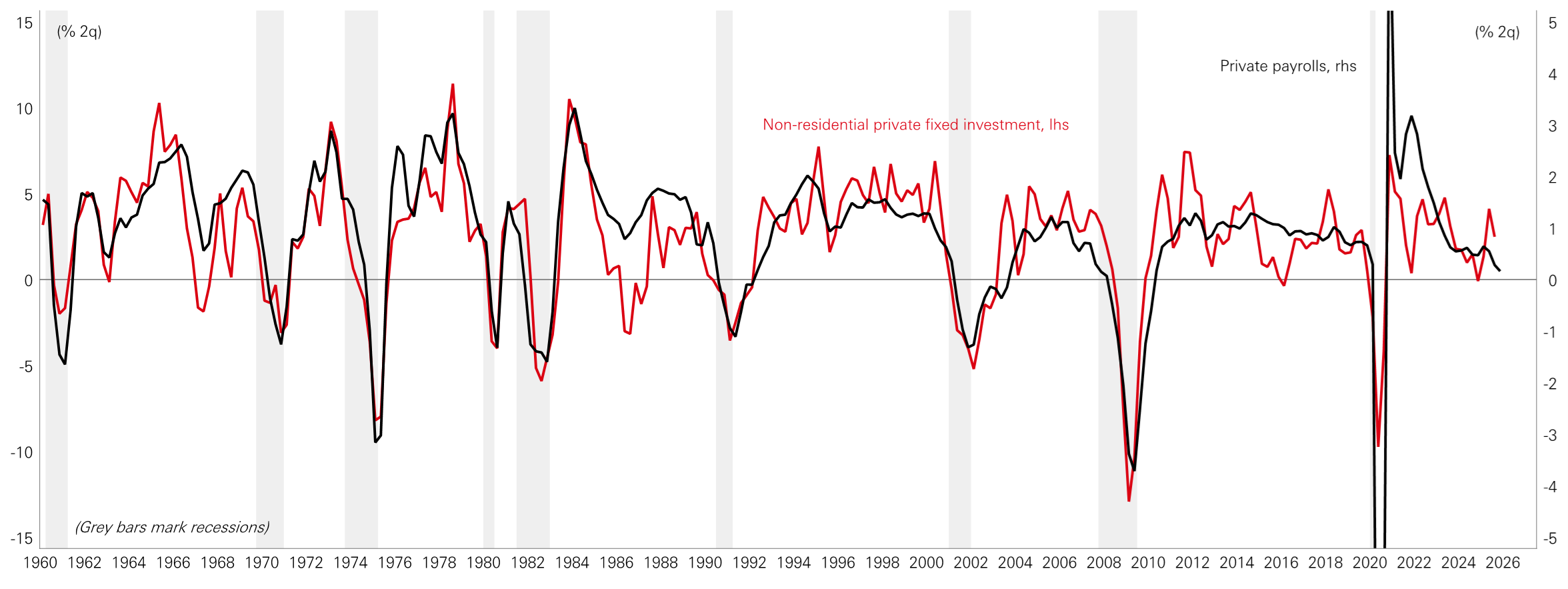

Historically, investment and employment have tended to move together, both being a form of corporate spending, but labour-market indicators have softened. Payroll gains slowed through H2 2025, with little private sector jobs growth outside of the healthcare sector.

Figure 4: Payrolls growth currently slowing

Click the image to enlarge

Source: Macrobond, HSBC AM, December 2025.

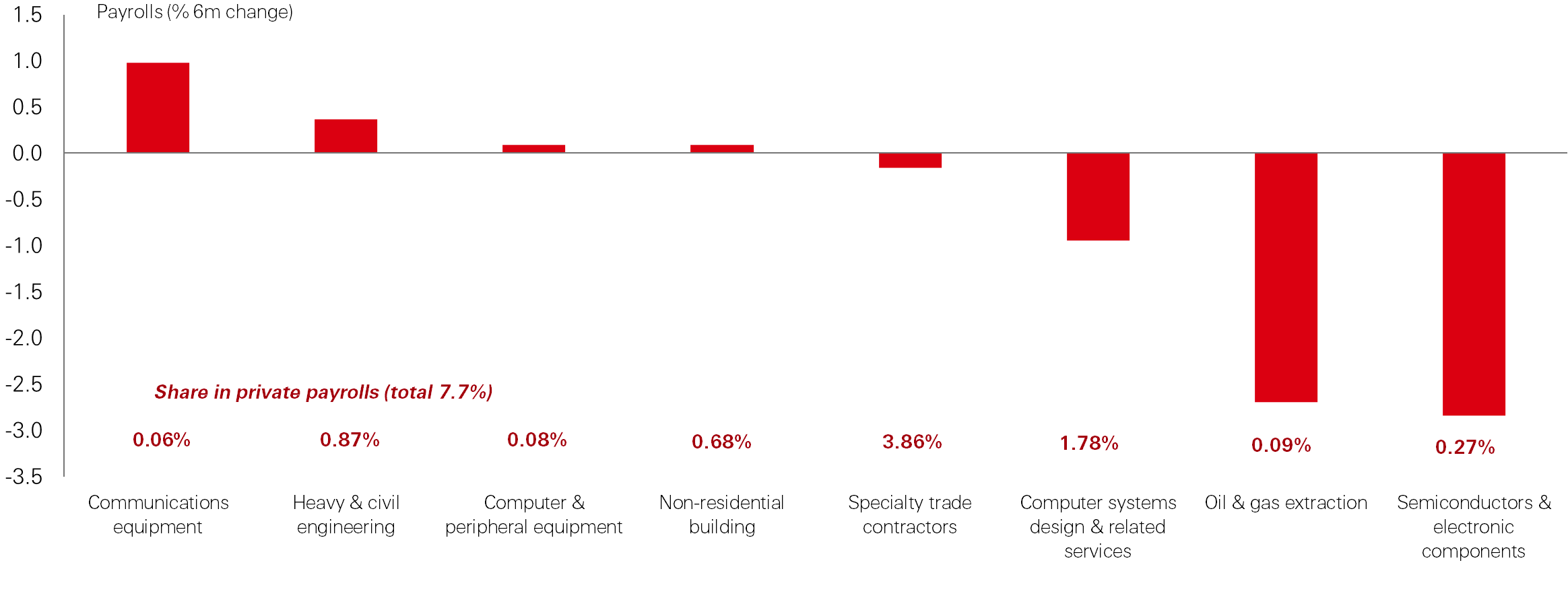

Sectors linked to data-centre construction – communications equipment, heavy civil engineering, computer and peripheral equipment, and non-residential building – account for around 7.7 per cent of private payrolls. While keeping in mind that much of the employment in these sector will not be impacted by tech capex, it is noteworthy that employment growth in these categories has been limited. This highlights how capital-intensive the AI build-out is: it requires substantial spending, but the direct employment footprint is narrow.

Figure 5: AI is capital intensive

Click the image to enlarge

Source: Macrobond, HSBC AM, December 2025.

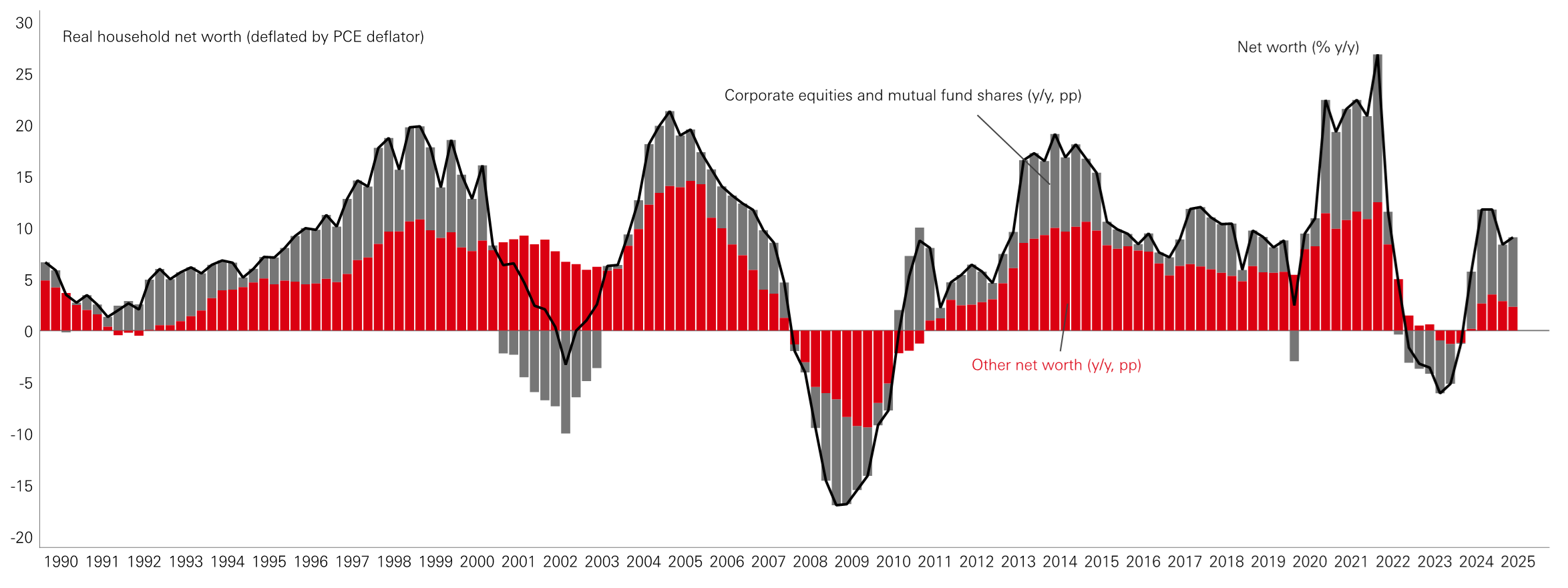

For many households, the benefits of the AI boom are muted. Strong gains in equities and mutual funds have supported net worth for wealthier households, who hold most financial assets. But real household net worth, adjusted for inflation, is not unusually elevated. Housing wealth is much more important for lower- and middle-income households, and the stagnant housing market has limited the gains for this asset in recent years.

Figure 6: Stronger wealth effect requires rapid equity price rises or housing recovery

Click the image to enlarge

Source: Macrobond, HSBC AM, December 2025.

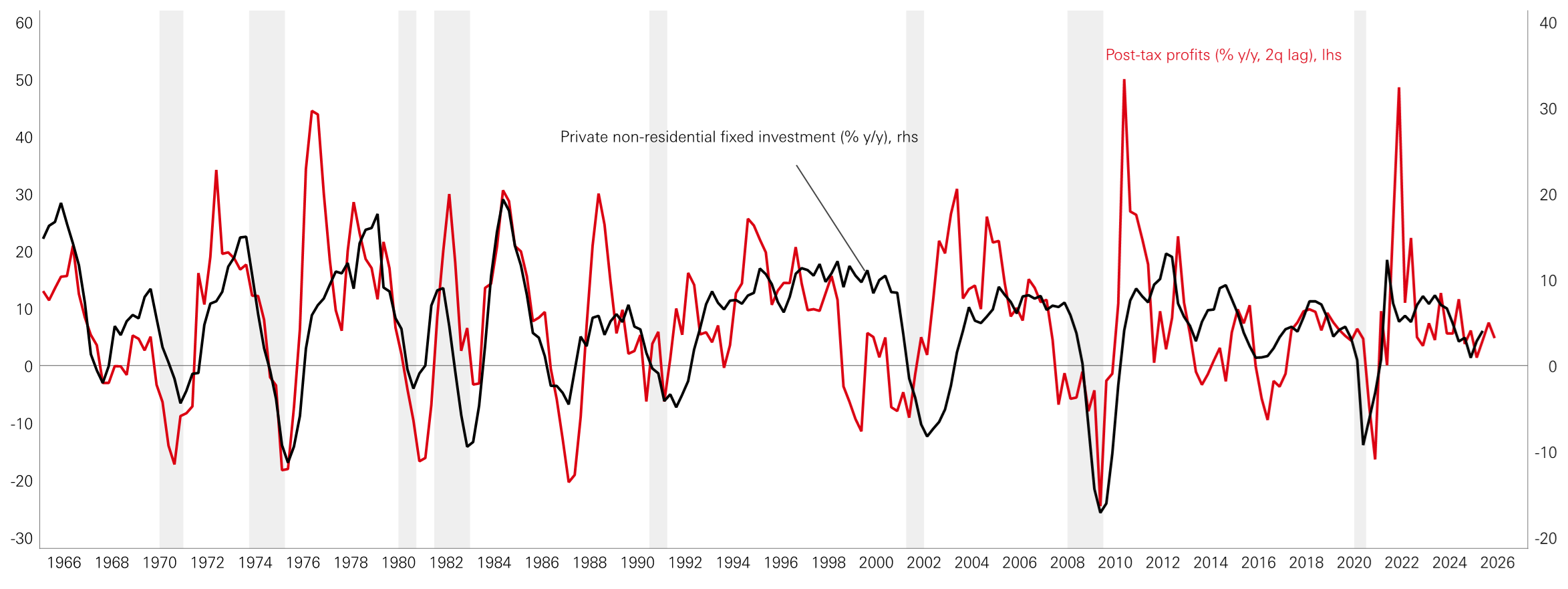

Monitoring profit performance is critical for assessing whether the AI boom continues to support the cycle or begins to fade. Historically, profits have led both investment and employment. Profit expectations for hyperscalers remain high, providing a foundation for elevated capex. The contrast with the late 1990s is notable: then, strong investment growth occurred despite weaker profit trends, driven by optimism about future returns. Today, profit growth is firmer, but expectations are also more demanding. Any disappointment could dampen investment plans, labour demand and equity valuations, with knock-on effects for consumption.

Figure 7: Late 1990s was the exception – could this time be another exception?

Click the image to enlarge

Source: Macrobond, HSBC AM, December 2025.

Generative AI is being adopted far faster than previous technological innovations, powered by the expectation of large productivity gains, and the race for AI leadership amongst the leading technology firms. Its potential depends on the rate of capital deepening, effective integration into workflows, and the associated labour market displacement.

Previous general-purpose technologies – from steam power and railways to automobiles and information technology – have typically followed a similar pattern: a phase of heavy infrastructure build-out to create capacity to meet expected future demand, followed by an assessment of whether this demand is realised. The ICT boom of the late 1990s/early 2000s saw extensive overbuild, much of it ultimately written down, yet the productivity dividends materialised later, once the capital stock was in place and business processes adapted. Generative AI in a similar fashion, is currently in the first phase and moving gradually into the second phase of enterprise adoption. Capital spending on models, data centres and supporting infrastructure is already substantial, but how this translates into sustained higher productivity will depend on how effectively the technology diffuses into enterprise workflows and the pace of widespread adoption.

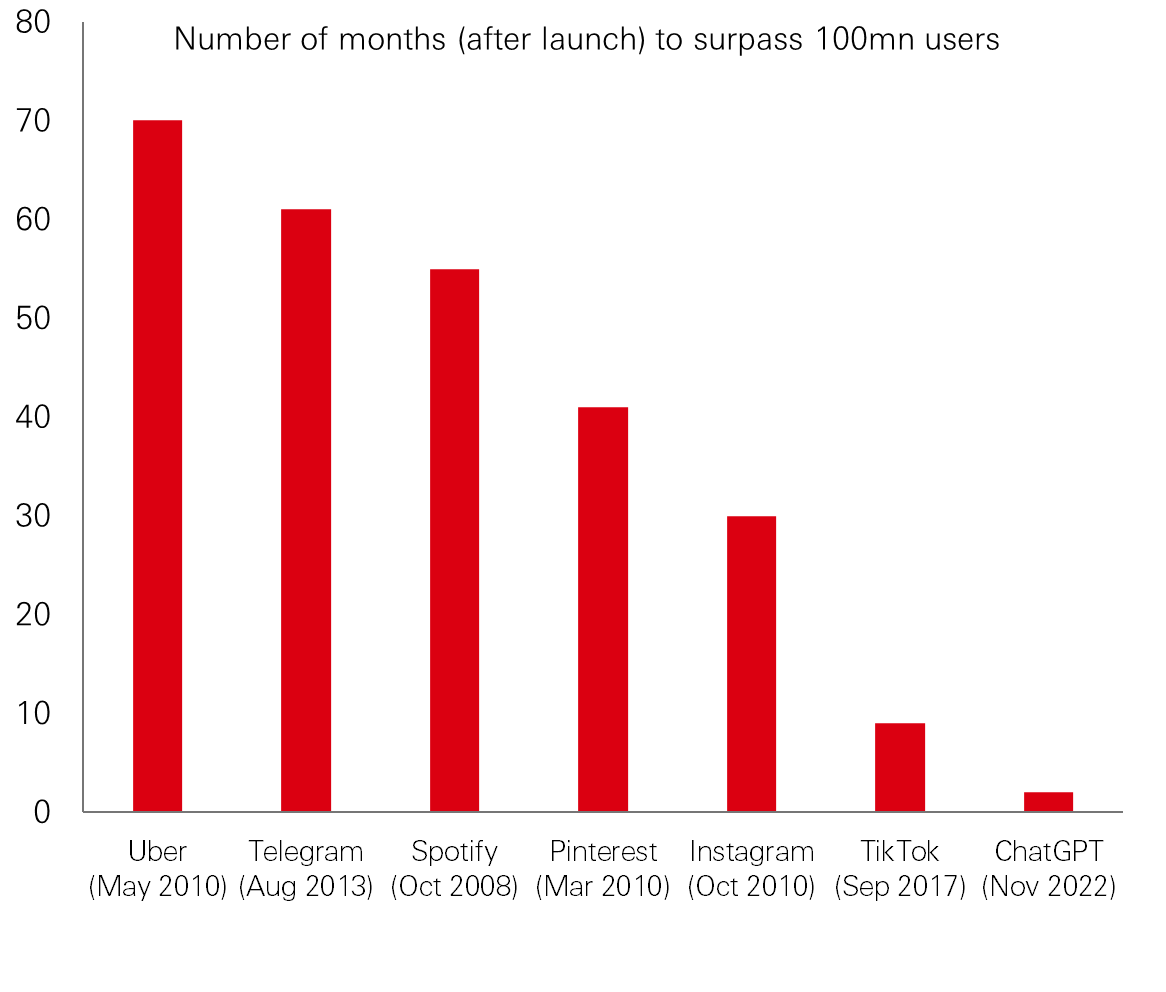

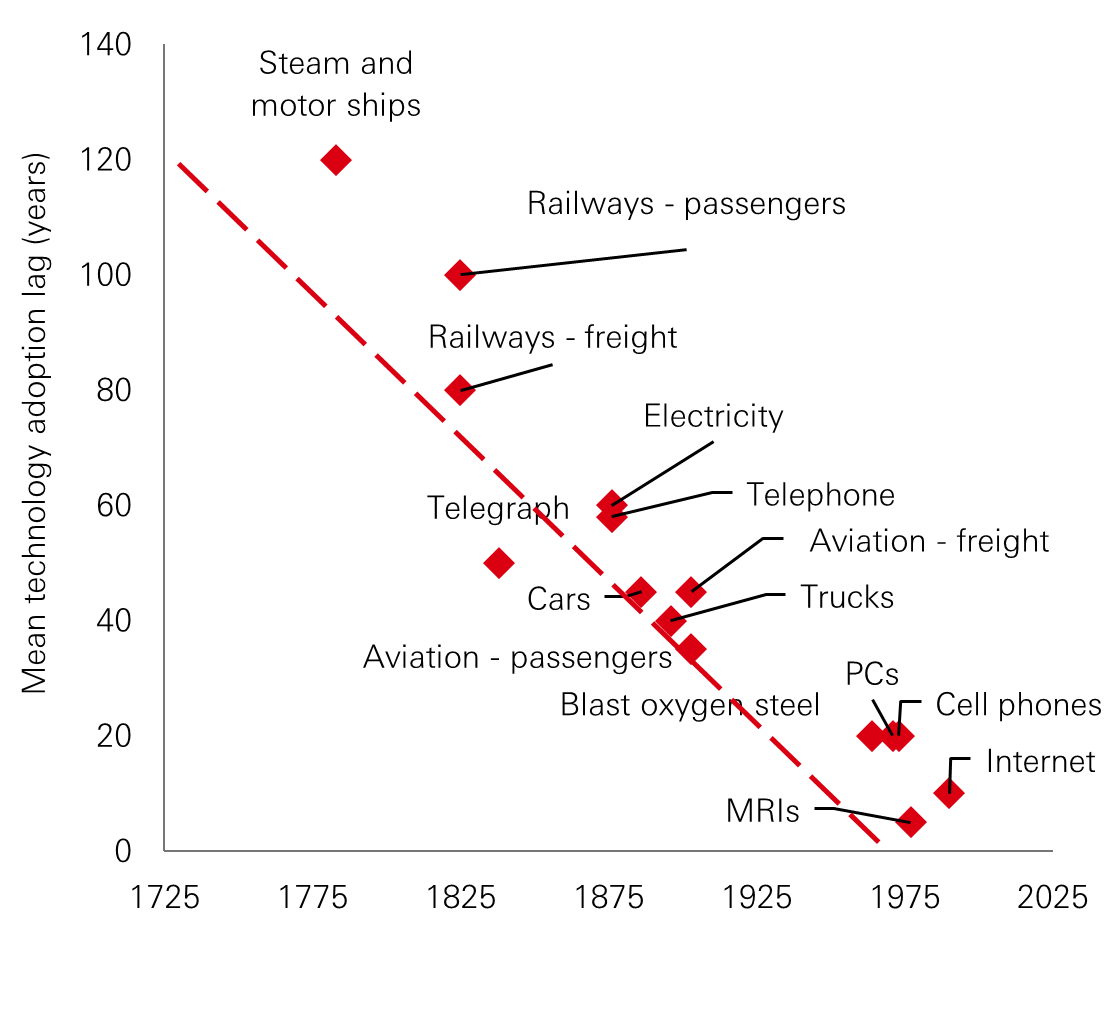

The current cycle nonetheless has some distinctive features. Unlike the dotcom era, the expansion is concentrated among a few incumbents with relative balance-sheet resilience and thus far has been financed primarily through internal cash. This reduces the likelihood of a classic, credit-driven bubble; even if individual assets could eventually be stranded if demand disappoints. The speed of development is also striking, with the adoption of technologies such as the telephone and motorships taking decades; the internet became mainstream in roughly a decade. By contrast, generative AI applications have reached mass user bases within months, supported by existing cloud infrastructure and its clear perceived utility, which reduces some of the purely speculative elements that may have characterised past bubbles.

Figure 8: OpenAI’s ChatGPT reached 100mn users in two months after launch

Click the image to enlarge

Figure 9: Trend suggests that the lag between innovation and adoption could be short

Click the image to enlarge

Source: Sensor Tower, ONS, Bureau of Labor Statistics, Macrobond, HSBC AM, December 2025.

The channels through which generative AI might lift productivity are clear in principle. At the micro level, the generalised nature of these tools means they can assist with a wide range of cases. These include document summarisation, coding, customer support, and digital-twin modelling for industrial systems. Aggregated to the macro level, this translates into labour upskilling (higher output per hour), capital deepening (more and better capital per worker) and improved total factor productivity as innovation is adopted at scale.

Some academic studies point to large labour productivity gains over the next decade, while more conservative estimates sit in the 5-10 per cent range. Whilst the mean of these projections is directionally positive, the dispersion highlights the core issue: uncertainty. The corporate survey data shares a similar ambiguity. From a macroeconomic standpoint, this wide variance reduces confidence that GenAI will be transformational in the near term. Historically, productivity inflections from general-purpose technologies tend to emerge only after complementary capital, skills, and management practices adapt, and often with a lag.

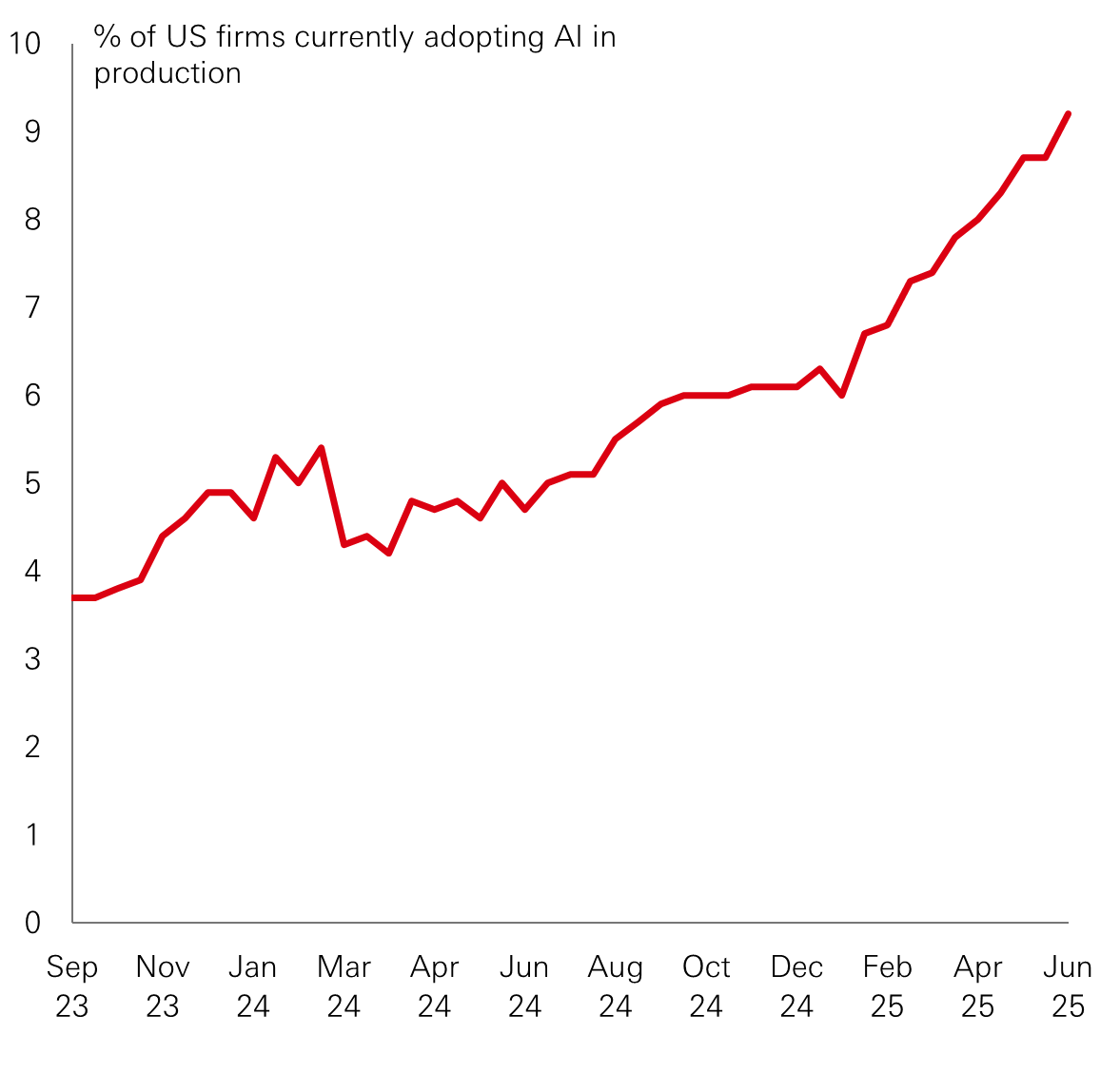

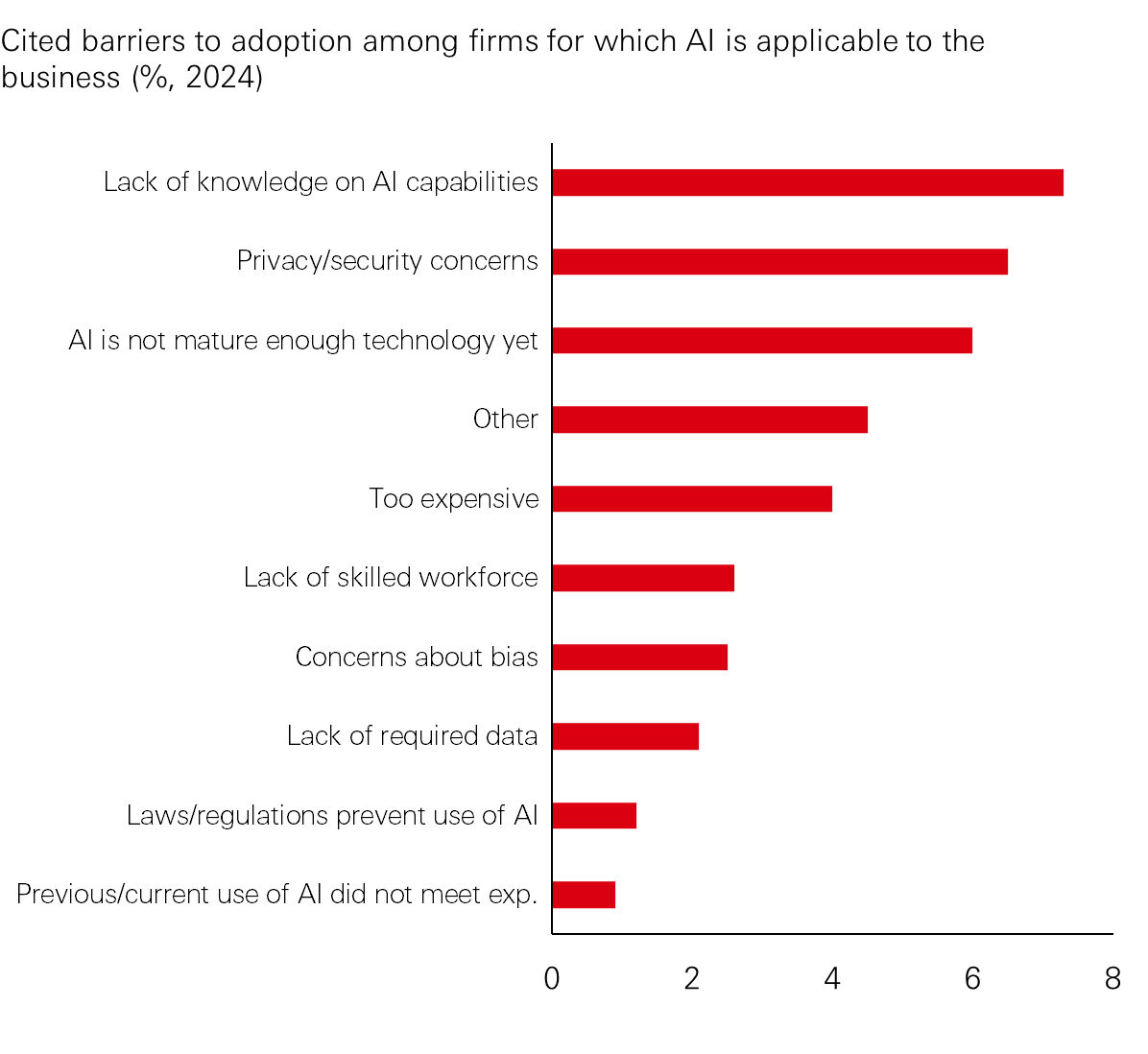

The main constraint at this juncture is neither investment nor model power, but in the challenges of enterprise absorption. Around 10 per cent of US firms are estimated to have AI in production, yet a relatively small fraction of pilots have translated into visible impact on profitability. Projects often stall at the proof-of-concept stage, held back by knowledge gaps on system capabilities, mis-specified use cases, security and privacy concerns, and difficulties integrating AI into existing workflows and governance. This is a classic diffusion issue: the technological frontier moves quickly, but the median firm is slowed by risk aversion, skills constraints and misaligned capital-allocation. Until organizations can adapt, AI’s contribution to aggregate productivity may remain marginal, even as infrastructure investment continues at record pace.

Figure 10: AI adoption has accelerated

Click the image to enlarge

Figure 11: Frictions emerge

Click the image to enlarge

Source: MIT, Census Bureau, HSBC AM, December 2025.

From a labour market perspective, some worker displacement is inevitable, consistent with past technological shifts, but some sectors are more exposed than others. Language- and code-intensive functions are the most exposed, while on-site manual work is less affected. Early adjustments are appearing more in hiring than in wages, as firms re-shape entry-level roles and shift some tasks towards more experienced staff who oversee AI-enabled processes. Over longer horizons, the balance between displacement and the creation of new, AI-complementary tasks will determine how much of the productivity premium is converted into higher incomes and employment rather than simply lower headcounts in specific job categories.

Implications for fixed income markets

For fixed income investors, the US AI investment cycle is shaping sector dynamics and influencing the rates outlook. AI-related companies are experiencing different balance sheet trends due to ongoing investment, while other sectors are more exposed to higher interest rates.

This means credit risks are becoming differentiated. AI-linked issuers may face risks tied to the timing and effectiveness of their investments, whereas non-AI sectors are more affected by rate pressures. Overall, steady economic growth from AI capex has reduced the likelihood of aggressive rate cuts, but investors should expect sector-specific credit challenges rather than broad-based risks.

As the cycle matures, careful issuer selection will be important, with attention to how each sector responds to both the AI investment wave and the broader rate environment. Investors should also consider how AI-driven companies are managing their capital allocation, as elevated spending on research, development, and infrastructure could impact leverage and liquidity metrics in the near term. Conversely, sectors less involved in the AI boom may need to adapt to tighter financial conditions and shifting consumer preferences, which could pressure margins and lead to increased refinancing risk.

Furthermore, the evolving regulatory landscape around AI and data usage may introduce additional uncertainties, affecting both credit profiles and long-term growth prospects. Investors will benefit from a nuanced approach, focusing on issuers with the flexibility to navigate both technological disruption and macroeconomic headwinds. In this environment, active portfolio management and ongoing sector analysis will be key to identifying resilient credits and capturing opportunities as the AI investment cycle continues to unfold.

Source: HSBC Asset Management, February 2026. The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security.