China in charts - II

Taking the pulse: China’s healthcare sector

The significance of China’s healthcare market

In our last “China in charts”, we illustrated how consumption and innovation are transforming China. In this edition, we continue to focus on China’s new economy, by narrowing into the nation’s healthcare industry. Through easy-to-understand charts, we illustrate why the remarkable growth of China’s healthcare is expected to continue and how innovation is increasingly being built into the sector’s DNA. Below we highlight key takeaways from the charts that follow:

- Rapidly evolving socio-economic factors and ongoing institutional support have catalysed the role of healthcare in China, placing the sector in a favourable position for continued growth

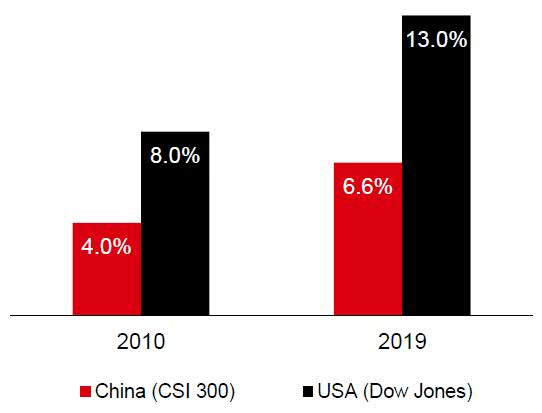

- With China undergoing the transition from an investment led economy to a consumption-driven one, new economy sectors – including technology, healthcare and consumer discretionary – have seen their equity index weight increase over the years

- Bottom up equity investors can potentially capitalise on the structural changes occurring within China’s healthcare sector as leading healthcare companies are increasingly placing more focus on innovation and moving up the value chain through research and development

- HSBC Global Asset Management’s China equity and Asia ex Japan regional equity strategies invest in both offshore and onshore healthcare opportunities

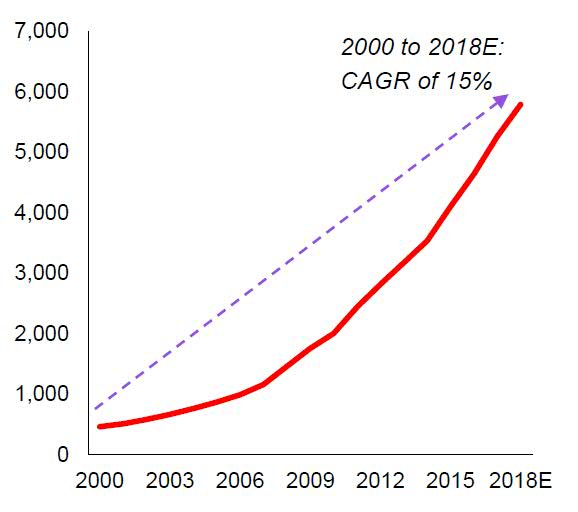

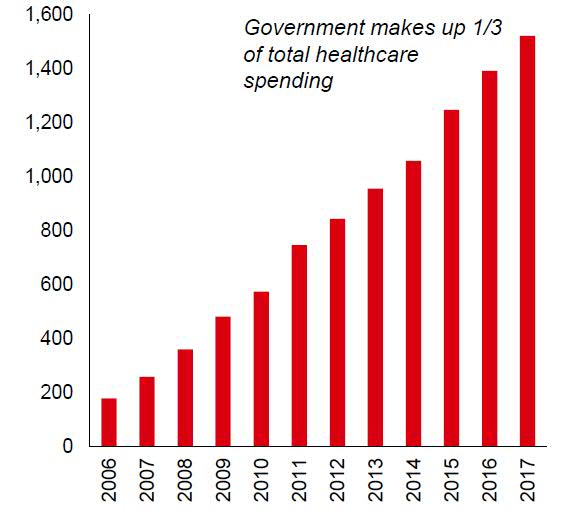

China healthcare’s extraordinary growth

China’s healthcare expenditure has grown at an extraordinary rate

China healthcare expenditure (RMB billion)

Healthcare industry has grown to more than 10 subsectors

Biotech innovator

First to market biosimilar drugs / generic

Contract research organizations (CRO)

Online services / Telemedicine

Diversified pharma

Specialty hospitals

Medical devices

Traditional Chinese medicine

Marketing / in-license

Distribution

General hospitals

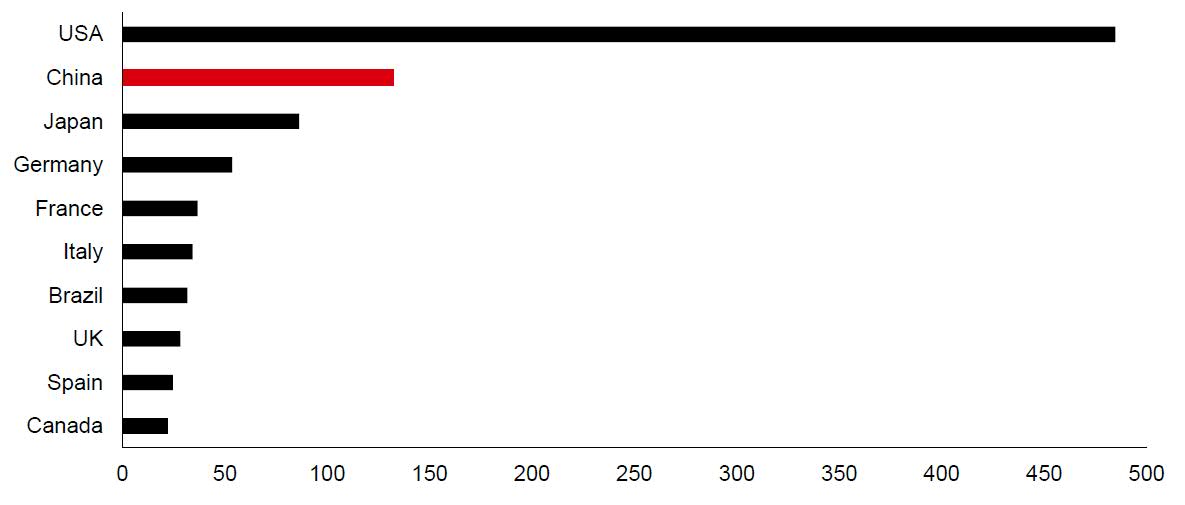

China’s pharmaceutical market is the second largest in the world

2018 spending on medicine (USD billion)

Source:

1. National Bureau of Statistics PRC, HSBC Global Asset Management, as of May 2019

2. JP Morgan, HSBC Global Asset Management, as of May 2019

3. IQVIA Institute for Human Data Science as of January 2019

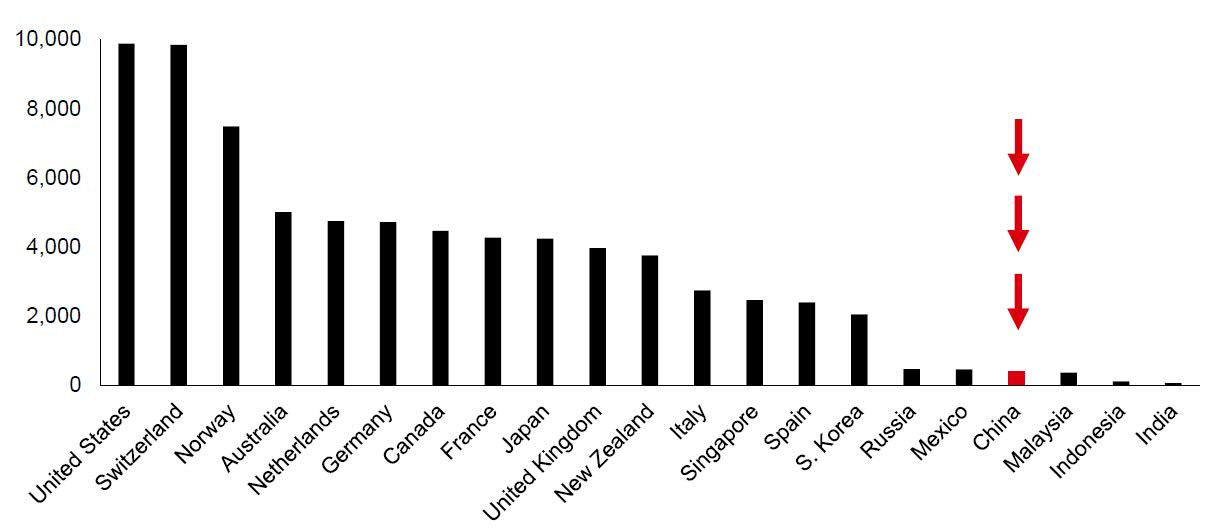

High potential to grow from relatively low levels

China’s healthcare expenditure per capita lags behind other major markets

Healthcare expenditure per capita (USD)

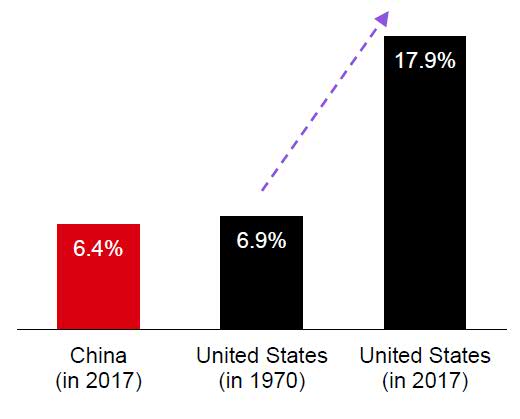

China’s healthcare spending is comparable to that of the U.S. in the 1970s

Healthcare expenditure (% of GDP)

Healthcare representation in China’s equity market is low but rising

Healthcare sector weight in index

Source:

1. World Health Organization, latest available data as of May 2019, based on 2016 data. WHO’s comprehensive and comparable database on health spending for 190 countries is updated annually and released in December of each year with a 2-year lag

2. National Bureau of Statistics PRC, U.S. Bureau of the Census, latest available data as of May 2019

3. Bloomberg as of May 2019

Healthcare sector has strong government support

Substantial government spending on healthcare

China government healthcare expenditure (RMB billion)

Loosening restrictions on foreign ownership has boosted investment

Foreign direct investment actually utilized in China’s health, social security and social welfare (USD million)

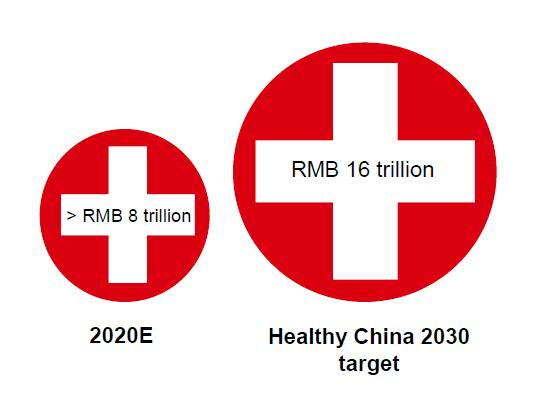

“Healthy China 2030” targets to grow health services market to RMB 16 trillion

Size of health services market

Biotech and high tech medical devices are a national priority

“Made in China 2025” - 10 strategic sectors

- New advanced IT

- Automated machine tools & robotics

- Aerospace and aeronautical equipment

- Maritime equipment & high tech ships

- Modern rail transport equipment

- New-energy vehicles & equipment

- Power equipment

- Agricultural equipment

- New materials

- Biotech and high tech medical devices

Source:

1. National Bureau of Statistics PRC, latest available data as of May 2019

2. Ministry of Commerce, as of May 2019

3. NHFCP as of January 2019

4. “Made in China 2025” action plan as announced by The State Council, PRC in May 2015

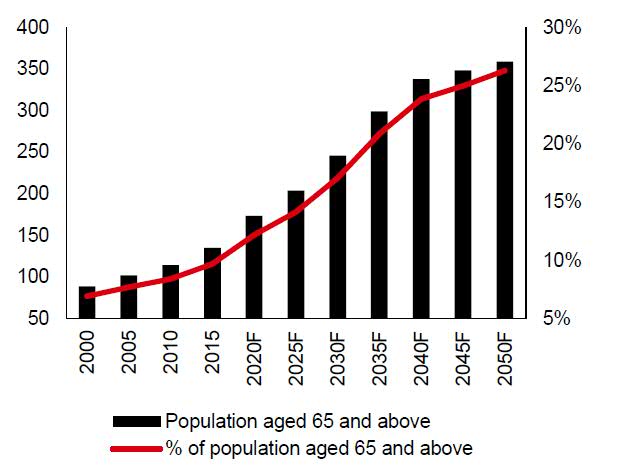

Demographic trends create immense demand for healthcare

Aging population adds to healthcare demand

|

Population aged 65 and above (million) in China |

% of population aged 65 and above in China |

China has the largest diabetic population in the world

Diabetic (adult)

population as % of world

Adults with diabetes

114 million

Prevalence of diabetes

10.9%

China’s diabetic patients as % of world

27%

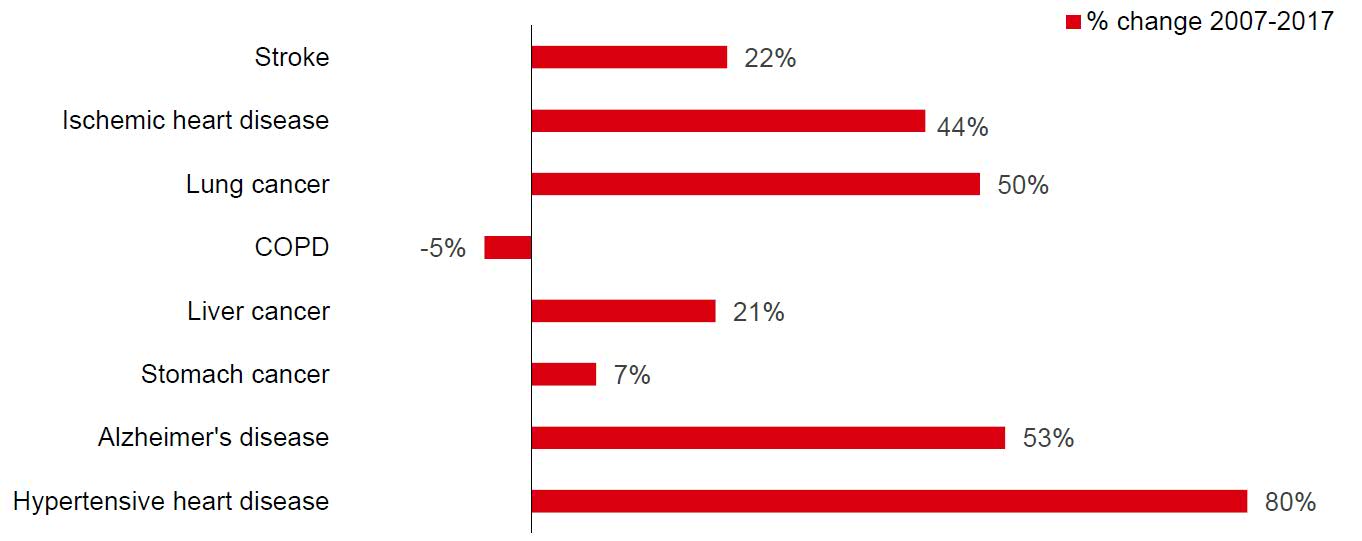

Rapid rise in chronic diseases

Of the top 10 causes of premature deaths in 2017 in China, eight are caused by non-communicable diseases

Listed by order; bar shows % change from 2007 to 2017

Source:

1. United Nations World Population Prospects 2017

2. International Diabetes Federation 2017

3. Institute for Health Metrics and Evaluation, as of 2019

Improvements in China’s healthcare are pushing the industry forward

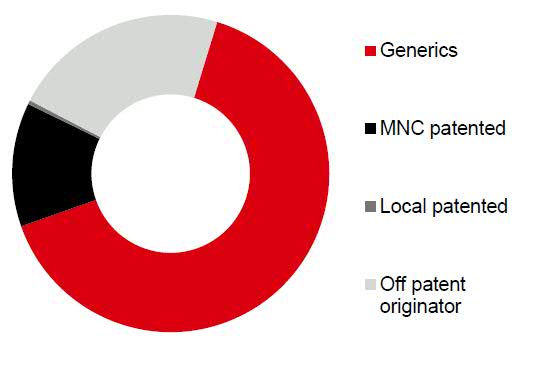

Although China’s pharma market is at an early stage and still dominated by generics…

Breakdown of China’s pharmaceutical market

(excluding Traditional Chinese Medicine)

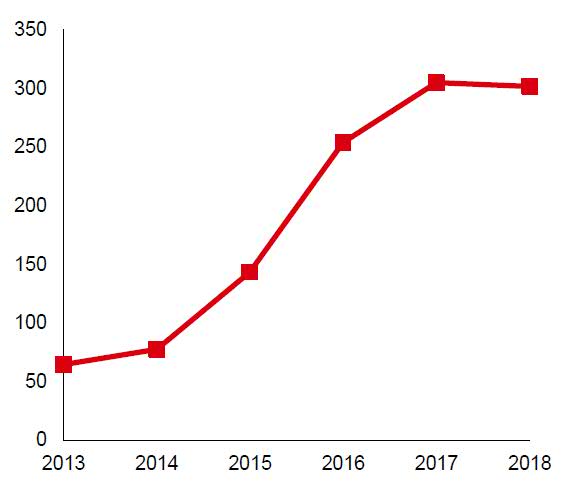

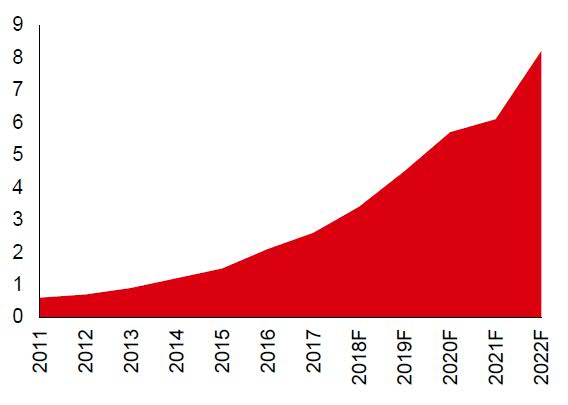

…Development of innovative drugs are on the rise

China biologics CRO market size (RMB billion)

Contract research organizations (CRO) provide research services to drug makers and are critical to the drug development process, including in drug discovery and drug research

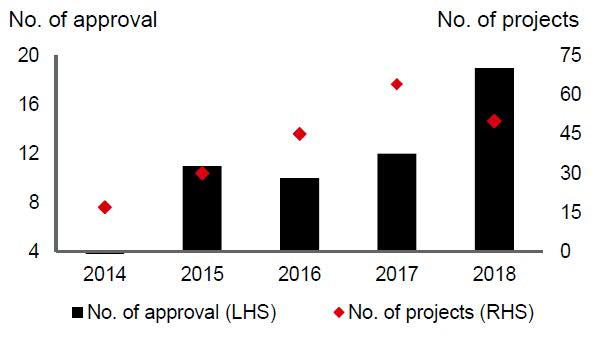

Innovation in medical devices is increasingly backed by policy support

Innovative medical device projects under China Food and Drug Administration (CFDA) green path

The CFDA green path was implemented in 2014 as a fast track of review and approval for innovative medical devices

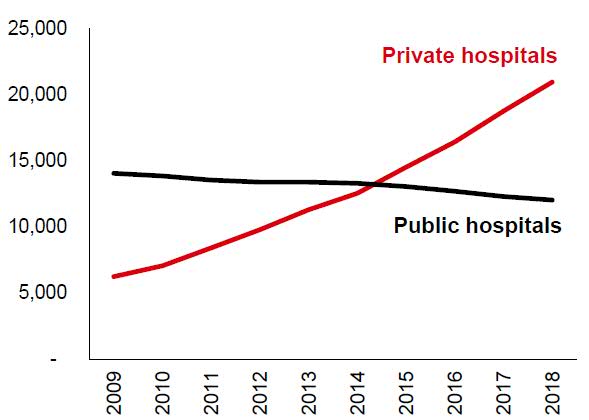

Policy has also been encouraging the private sector to expand its role in the system

Number of hospitals nationwide

Source:

1. JP Morgan as of May 2019

2. Nomura, Frost & Sullivan, as of May 2019

3. China Medical Device Evaluation Center (CMDE), JP Morgan as of May 2019

4. National Health Commission of the PRC, as of May 2019

Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC accepts no liability for any failure to meet such forecasts, projections or targets. For illustrative purposes only.

Important information

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Global Asset Management at the time of preparation, and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Global Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. Past performance contained in this document is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in Emerging Markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Mutual fund investments are subject to market risks, read all scheme related documents carefully.

We accept no responsibility for the accuracy and/or completeness of any third party information obtained from sources we believe to be reliable but which have not been independently verified.

This document has not been reviewed by the Securities and Futures Commission.

Risk Warning

This page is prepared for general information purposes only and does not have any regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive it. This page does not constitute an offering document and should not be construed as a recommendation, an offer to sell or the solicitation of an offer to purchase or subscribe to any investment. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Global Asset Management (Hong Kong) Limited (“AMHK”) accepts no liability for any failure to meet such forecast, projection or target. AMHK has based on information obtained from sources it reasonably believes to be reliable. However, AMHK does not warrant, guarantee or represent, expressly or by implication, the accuracy, validity or completeness of such information.